Which of the characteristics put forth by Chaterji to describe the factor-based approach is/are correct? A. Only

Question:

Which of the characteristics put forth by Chaterji to describe the factor-based approach is/are correct?

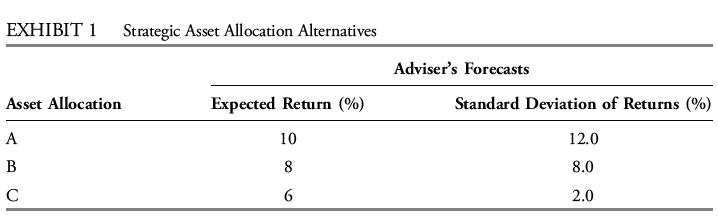

A. Only Characteristic 1 B. Only Characteristic 2 C. Both Characteristic 1 and Characteristic 2 Investment adviser Carl Monteo determines client asset allocations using quantitative techniques such as mean–variance optimization (MVO) and risk budgets. Monteo is reviewing the allocations of three clients. Exhibit 1 shows the expected return and standard deviation of returns for three strategic asset allocations that apply to several of Monteo’s clients.

Monteo interviews client Mary Perkins and develops a detailed assessment of her risk preference and capacity for risk, which is needed to apply MVO to asset allocation. Monteo estimates the risk aversion coefficient (λ) for Perkins to be 8 and uses the following utility function to determine a preferred asset allocation for Perkins:

![]()

Another client, Lars Velky, represents Velky Partners (VP), a large institutional investor with $500 million in investable assets. Velky is interested in adding less liquid asset classes, such as direct real estate, infrastructure, and private equity, to VP’s portfolio. Velky and Monteo discuss the considerations involved in applying many of the common asset allocation techniques, such as MVO, to these asset classes. Before making any changes to the portfolio, Monteo asks Velky about his knowledge of risk budgeting. Velky makes the following statements:

Statement 1: An optimum risk budget minimizes total risk.

Statement 2: Risk budgeting decomposes total portfolio risk into its constituent parts.

Statement 3: An asset allocation is optimal from a risk-budgeting perspective when the ratio of excess return to marginal contribution to risk is different for all assets in the portfolio.

Monteo meets with a third client, Jayanta Chaterji, an individual investor. Monteo and Chaterji discuss mean–variance optimization. Chaterji expresses concern about using the output of MVOs for two reasons:

Criticism 1: The asset allocations are highly sensitive to changes in the model inputs.

Criticism 2: The asset allocations tend to be highly dispersed across all available asset classes.

Monteo and Chaterji also discuss other approaches to asset allocation. Chaterji tells Monteo that he understands the factor-based approach to asset allocation to have two key characteristics:

Characteristic 1: The factors commonly used in the factor-based approach generally have low correlations with the market and with each other.

Characteristic 2: The factors commonly used in the factor-based approach are typically different from the fundamental or structural factors used in multifactor models.

Monteo concludes the meeting with Chaterji after sharing his views on the factor-based approach.

Step by Step Answer: