Cost-volume-earnings analysis (breakeven analysis) is used to determine and express the interrelationships of different volumes of activity

Question:

Cost-volume-earnings analysis (breakeven analysis) is used to determine and express the interrelationships of different volumes of activity (sales), costs, sales prices, and sales mix to earnings. More specifically, the analysis is concerned with what will be the effect on earnings of changes in sales volume, sales prices, sales mix, and costs.

{Required:}

a. Certain terms are fundamental to cost-volume-earnings analysis. Explain the meaning of each of the following terms:

1. Fixed costs.

2. Variable costs.

3. Relevant range.

4. Breakeven point.

5. Margin of safety.

6. Sales mix

b. Several assumptions are implicit in cost-volume-earnings analysis. What are these assumptions?

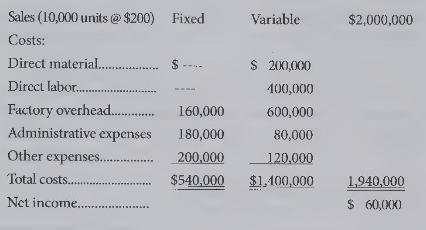

c. In a recent period Zero Company had the following experience:

Each item below is independent.

1. Calculate the breakeven point for Zero in terms of units and sales dollars. Show your calculations.

2. What sales volume would be required to generate a net income of \(\$ 96,000\) ? Show your calculations.

3. What is the breakeven point if management makes a decision, which increases fixed costs by \(\$ 18,000\) ? Show your calculations.

Step by Step Answer:

Cost Accounting For Managerial Planning Decision Making And Control

ISBN: 9781516551705

6th Edition

Authors: Woody Liao, Andrew Schiff, Stacy Kline