Question: CTD Ltd has two divisions FD and TM. FD is an iron foundry division which produces mouldings that have a limited external market and

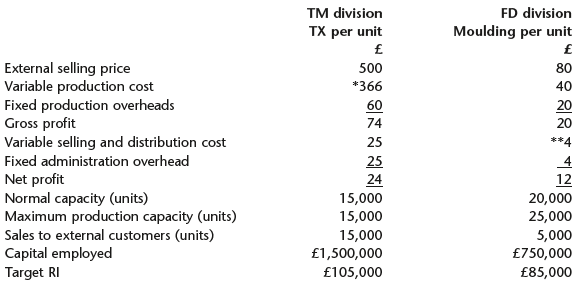

CTD Ltd has two divisions – FD and TM. FD is an iron foundry division which produces mouldings that have a limited external market and are also transferred to TM division. TM division uses the mouldings to produce a piece of agricultural equipment called the ‘TX’ which is sold externally. Each TX requires one moulding. Both divisions produce only one type of product. The performance of each divisional manager is evaluated individually on the basis of the residual income (RI) of his or her division. The company’s average annual 12% cost of capital is used to calculate the finance charges. If their own target residual income is achieved, each divisional manager is awarded a bonus equal to 5% of his or her residual income. All bonuses are paid out of head office profits. The following budgeted information is available for the forthcoming year:

* The variable production cost of the TX includes the cost of an FD moulding.** External sales only of the mouldings incur a variable selling and distribution cost of £4 per unit.FD division currently transfers 15,000 mouldings to TM division at a transfer price equal to the total production cost plus 10%.

Fixed costs are absorbed on the basis of normal capacity.

Required:(a) Calculate the bonus each divisional manager would receive under the current transfer pricing policy and discuss any implications that the current performance evaluation system may have for each division and for the company as a whole. (7 marks)(b) Both divisional managers want to achieve their respective residual income targets. Based on the budgeted figures, calculate:(i) the maximum transfer price per unit that the divisional manager of TM division would pay.(ii) the minimum transfer price per unit that the divisional manager of FD division would accept. (6 marks)(c) Write a report to the management of CTD Ltd which explains, and recommends, the transfer prices that FD division should set in order to maximize group profits. Your report should also:

• consider the implications of actual external customer demand exceeding 5,000 units; and

• explain how alternative transfer pricing systems could overcome any possible conflict that may arise as a result of your recommended transfer prices.

your answer must be related to CTD Ltd. You will not earn marks by just describing various methods for setting transfer prices. (12 marks) (Total = 25 marks)

Step by Step Solution

3.37 Rating (166 Votes )

There are 3 Steps involved in it

ANSWER a Bonus Calculation and Implications TM divisions RI Net profit Target RI Capital Employed 100 24 105000 750000 100 796500 FD divisions RI Net ... View full answer

Get step-by-step solutions from verified subject matter experts