In common with the rest of the National Health Service, Freeshire Hospital Trust is having to cope

Question:

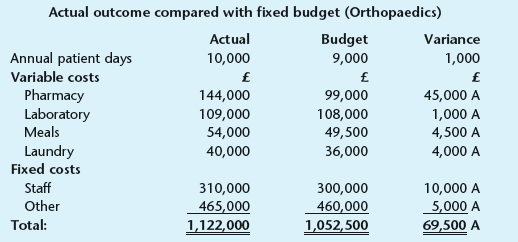

The chief executive is outraged that every variable cost variance is adverse and is, in his view, a demonstration of completely ineffective cost control. Moreover, he is becoming increasingly concerned, not only about the failure to keep within previous budgets, but also by the new budgets for next year which are being proposed by the department managers. Mindful of his lack of financial expertise, the chief executive has decided to bring in a new financial director. The latter has been recruited to investigate the problems with the newly decentralized system and to put forward some proposals on future development. In his initial meetings with senior staff the new financial director obtained the following quotes:

Chief executive

I don€™t understand it. I didn€™t have these problems in my last organization. People understood the system and its objectives. People didn€™t play games, they didn€™t build €˜fudge factors€™ into their budgets. I don€™t see any budget reductions made in the light of our cost-saving information technology investment program. As for the new budget reports, I never know if the variances are real or just a matter of poor phasing of expenditure across the year. I also need more warning of how the year is developing. I want realistic budget figures with a little to stretch people and we have got to have a budget which fi ts our corporate objectives. Or maybe we should scrap the budget altogether and put one of these new balanced scorecards in its place?

Department manager

I€™m not going to put another brave budget forward after last year. Last year they published a league table of performance against budget and I came bottom. This year I will be giving myself plenty of slack. Next year€™s budget is this year€™s plus 15 per cent. I am sure they will knock 5 per cent off straight away even without looking at the budget submission. As for the forms, reports and budget procedure, they just take too long. Every month I have to fill this massive form covering what I have spent and even what bills I am going to pay in the future. This is a system designed by accountants for accountants. I€™ve got real work to do. In any case, I never get any feedback on the figures until months later.

Chief accountant

We produce monthly reports with actual spend against budget and never get any credible responses explaining the variances. All we seem to get is complaints about the way we have phased the budgets. They don€™t understand it€™s not down to us that their budgets are cut €“ not that it makes any difference, they never know if they are overspent or not. All levels of management have poor budgetary discipline, the budget is there to be complied with. They€™re always being creative; it€™s amazing what gets classed as training when that line is underspent! How can I stop them from messing around with my accounts? Most managers aren€™t rigorous enough in defining their budget assumptions, especially the board; I keep telling them it€™s to protect them, especially when things go wrong.

A clinical director

I am fed up with this budgetary control system, it just gives me a headache. Firstly, it€™s too complex. Secondly, I get the analysis of my expenditure five or six weeks after the month end. Thirdly, I get no explanation of the variances! My staff have also become adept at beating the system. I found one spending her budget on non-essentials just so it wouldn€™t get cut next year. Another overspent manager negotiated with a local supplier to post-date an invoice into next year. Where will it end?

Tasks:

1. Discuss the chief executive€™s opinion that the orthopaedics budget is indicative of a complete lack of control. Show the calculations of any figures you use to substantiate your argument. (20 marks)

2. Explain what you understand by €˜budget games€™. Using the Free shire case where possible, give examples of these games. (28 marks)

3. State the main purpose of balanced scorecards. Also, list their subsidiary benefits/ objectives. Compare the concept of lead/lag perspectives in €˜for-profit€™ and €˜not-for-profit€™ organizations. (18 marks)

4. Design a balanced scorecard for use in a not-for-profit hospital. Give two goals and two performance indicators for each of the perspectives. (Do not show targets.) (34 marks) (Total 100 marks)

Step by Step Answer:

1 The adverse variable cost variances shown in the question are due to the actual activity level being greater than that used to create the original budget this is an unfair comparison The actual perf...View the full answer

Managerial Accounting Decision Making and Performance Management

ISBN: 978-0273764489

4th edition

Authors: Ray Proctor