Question:

Notwithstanding the discussion in Section 12.1.4, since we forecast based on Libor, the martingale equation only holds for risky discounting at the credit-worthiness of Libor counterparts. As such, OIS discounting induces a quanto correction. In the developed world, it is common for interest rates to be lowered in times of crisis to simulate growth. As such, what should the direction of the quanto correction be? (Note that this is really just a theoretical discussion, since such a quanto correction is accounted for by market quotes which are based on Libor forecasting and OIS discounting.)

Section 12.1.4,

Transcribed Image Text:

From our discussion earlier, it can be seen that funding is no longer

an after-thought in the pricing of derivatives. It should be clear from

the earlier graphs of the OIS spread and Libor basis spreads that

funding spreads are not constant. Stochastic funding can lead to

increased volatility of an underlying, and thus can increase the price

of an option.

More interestingly, stochastic funding can even affect the for-

ward price of an underlying, if the funding spread is correlated with

the underlying. This is not a far-fetched point. Funding spreads

(over the risk-free rate) are likely to be highest in times of finan-

cial crisis. In safe haven (e.g. G7) economies (that are not on the

brink of default), central banks will attempt to stimulate economic

growth by cutting interest rates. So, funding spreads can be quite

negatively correlated with interest rates. Alternatively, in a non-safe

haven economy on the brink of collapse, interest rates may need to

be raised in times of crisis either as borrowers will no longer lend or

because international bodies (e.g. the International Monetary Fund)

demand such measures as a condition for financial assistance. So, cor-

relation between funding spreads and interest rates can be positive

instead.

Piterbarg [Pit10] shows that stochastic funding spreads can lead

to a quanto effect on the forward price of an underlying. Let Xt be

the value of an underlying, rt be the risk-free rate for collateralised

borrowing, r be the (risky) rate for uncollateralised borrowing by

some counterparty A (which could but need not be Libor-eligible),

and sr rt be the spread.

Consider a forward contract with maturity T and strike K with

a CSA-counterparty. Its value at time t is

Ele-Strudu ¹u (XT - K)],

so the fair value CSA-forward price of the asset is:

FCSA = ELerudu XT]/EX[e-² rudu]

ET [XT],

where we have changed from the risk-neutral measure to the

T-forward measure (with numeraire asset being the discount bond

with maturity T given by D(t, T) = E?[e-Serudu], and discounting

is based on the OIS curve).

Consider instead the same forward contract with counterparty

A (for which no CSA arrangement is in place). The value of the

forward is

Ele-Srdu (XT - K)].

So the fair value forward price is given by

FnoCSA = Eedu XT]/D¹(t, T)

=

where DA (t, T) E[e-du] is the discount curve for counter-

party A, and we have again changed from the risk-neutral measure

to the T-forward measure.

ET

Then the quanto adjustment to the forward rate as a consequence

of non-collateralised funding (from our counterparty A) is

Ele-Si rudu-ſi (r^-ru)du XT]/Dª(t,T),

D(t, T)

DA(t, T)

FnoCSA (t,T) - FCSA(t, T)

=

Correction (%)

D(t, T)

- B² [(D4-1²-1) X7]

=

e

x

XT

DA(t, T)

since we have

-Elle-

ET (D(t, T)

0.40

0.30

0.20

0 10

0.00

-0.100

-0.20

-0.30

-0.40

D(t, T) - sdu

DA(t, T)

e

- ST s du XT]

Et

B² [( DA(1t, T)

5(e-li sidu - El (e-f² sâ du)))

t, T))]

X (XT FCSA (t, T))

-

D(t, T) cov (e-fsdu, XT),

DA(t, T)

- S² s^ du] =

5

e-² at du _ 1) (XT - FOSA(t, T))]

-

10

du

1

Thus, we see that the correlation between the funding spread s and

the underlying XT induces a quanto adjustment on the fair forward

price in the non-CSA case (vis-à-vis the CSA case).

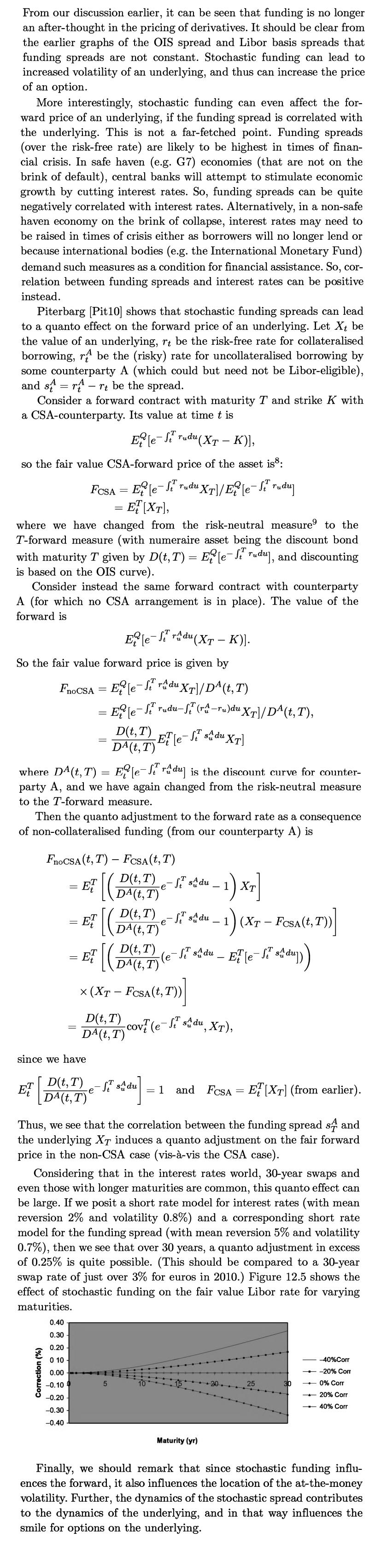

Considering that in the interest rates world, 30-year swaps and

even those with longer maturities are common, this quanto effect can

be large. If we posit a short rate model for interest rates (with mean

reversion 2% and volatility 0.8%) and a corresponding short rate

model for the funding spread (with mean reversion 5% and volatility

0.7%), then we see that over 30 years, a quanto adjustment in excess

of 0.25% is quite possible. (This should be compared to a 30-year

swap rate of just over 3% for euros in 2010.) Figure 12.5 shows the

effect of stochastic funding on the fair value Libor rate for varying

maturities.

and FCSA ETXT] (from earlier).

Maturity (yr)

-

20.

25

-40%Corr

-20% Corr

0% Corr

20% Corr

-40% Corr

Finally, we should remark that since stochastic funding influ-

ences the forward, it also influences the location of the at-the-money

volatility. Further, the dynamics of the stochastic spread contributes

to the dynamics of the underlying, and in that way influences the

smile for options on the underlying.