From the bond price representation formula (7.2.10), use Itos differentiation to show where R(t,T ) is the

Question:

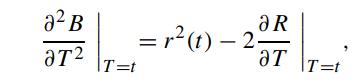

From the bond price representation formula (7.2.10), use Ito’s differentiation to show

where R(t,T ) is the yield to maturity. Also, try to relate the market price of interest rate risk λ(r,t) to ∂R/∂T |T =t.

where R(t,T ) is the yield to maturity. Also, try to relate the market price of interest rate risk λ(r,t) to ∂R/∂T |T =t.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Itos lemma is a powerful tool in stochastic calculus that allows us to find the differential of a fu...View the full answer

Answered By

OTIENO OBADO

I have a vast experience in teaching, mentoring and tutoring. I handle student concerns diligently and my academic background is undeniably aesthetic

3+ Reviews

10+ Question Solved

Related Book For

Question Posted: