Show that when a European option is currently out-of-the-money, then higher volatility of the asset price or

Question:

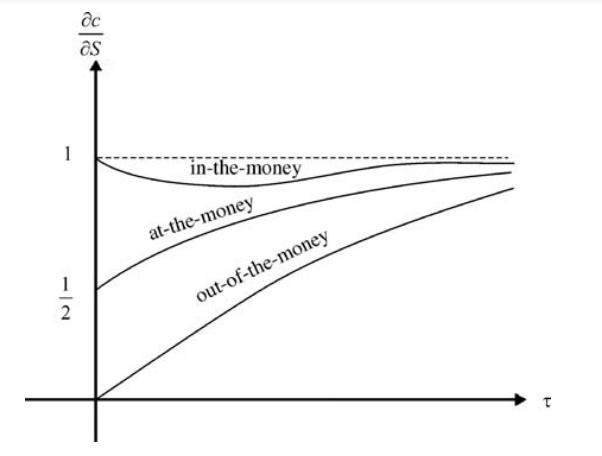

Show that when a European option is currently out-of-the-money, then higher volatility of the asset price or longer time to expiry makes it more likely for the option to expire in-the-money. What would be the impact on the value of delta? Do we have the same effect or opposite effect when the option is currently inthe-money? Also, give the financial interpretation of the asymptotic behavior of the delta curves in Fig. 3.4 at the respective limit τ → 0+ and τ → ∞.

Fig. 3.4

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

When a European option is outofthemoney OTM an increase in the volatility of the underlying assets price makes it more likely for the option to expire ...View the full answer

Answered By

Branice Buyengo Ajevi

I have been teaching for the last 5 years which has strengthened my interaction with students of different level.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: