Suppose an American put option is only allowed to be exercised at N time instants between now

Question:

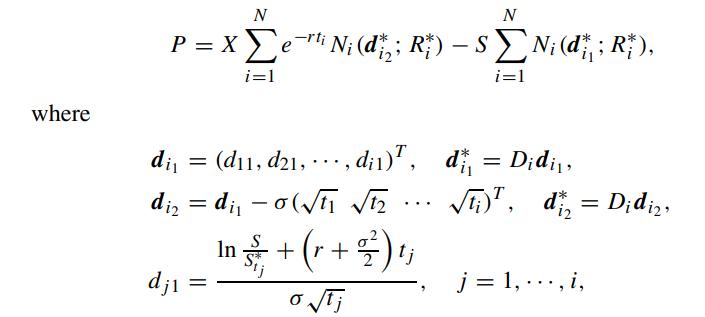

Suppose an American put option is only allowed to be exercised at N time instants between now and expiration. Let the current time be zero and denote the exercisable instants by the time vector t = (t1 t2 ··· tN )T. Let Ni(di; Ri) denote the i-dimensional multi-variate normal integral with upper limits of integration given by the i-dimensional vector di and correlation matrix Ri. Define the diagonal matrix Di = diag (1, ··· 1, −1), and let d∗i = Didi and R∗i = DiRiDi. Show that the value of the above American put with N exercisable instants is found to be (Bunch and Johnson, 1992)

and S∗tj is the optimal exercise price at tj . Also, find the expression for the correlation matrix Ri.

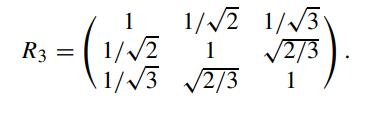

When N = 3 and the exercisable instants are equally spaced, the correlation matrix R3 is found to be

Step by Step Answer:

To derive the expression for the American put option with N exercisable instants lets follow the pro...View the full answer