The dynamic fund protection feature in an equity-linked fund product guarantees a predetermined protection level K to

Question:

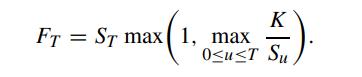

The dynamic fund protection feature in an equity-linked fund product guarantees a predetermined protection level K to an investor who owns the underlying fund. Let St denote the value of the underlying fund. The dynamic protection replaces the original value of the underlying fund by an upgraded value Ft so that Ft is guaranteed not to fall below K. That is, whenever Ft drops to K, just enough capital will be added by the sponsor so that the upgraded fund value does not fall below K.

(a) Show that the value of the upgraded fund at maturity time T is given by

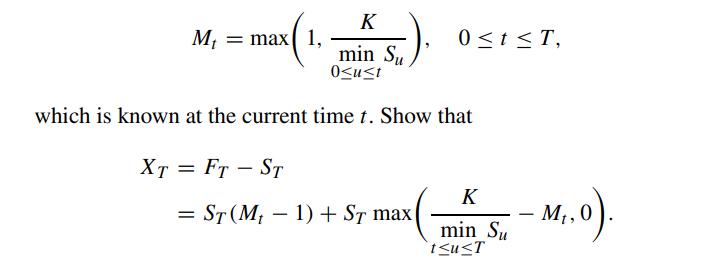

(b) Let XT denote the terminal value of the derivative that provides the dynamic fund protection. Define the lookback state variable

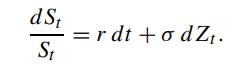

(c) Under the risk neutral measure Q, let the dynamics of St be governed by

(c) Under the risk neutral measure Q, let the dynamics of St be governed by

Show that the fair value of the dynamic fund protection is given by (Imai and Boyle, 2001)

![V(S, M, t) = EQ[XT] d = S[MN (d) 1] + = d3 = k+ (r + ) t O K + (1 - 1) Ke=](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/4/8/8/859655b669b2a8451700488855479.jpg)

Step by Step Answer: