ZIM Inc. (ZIM) is a high-technology company that develops, designs, and manufactures telecommunications equipment. ZIM was founded

Question:

ZIM Inc. (ZIM) is a high-technology company that develops, designs, and manufactures telecommunications equipment. ZIM was founded in Year 5 by Dr. Alex Zimmer, the former assistant head of research and development at a major telephone company. He and the director of marketing left the company to found ZIM. ZIM has been very successful. Sales reached $8.3 million in its first year and have grown by 80% annually since then. The key to ZIM's success has been the sophisticated software contained in the equipment it sells.

ZIM's board of directors recently decided to issue shares to raise funds for strategic objectives through an initial public offering of common shares. The shares will be listed on a major Canadian stock exchange. ZIM's underwriter, Mitchell Securities, believes that an offering price of 18 to 20 times the most recent fiscal year's earnings per share can be achieved. This opinion is based on selected industry comparisons.

ZIM has announced its intention to go public, and work has begun on the preparation of a preliminary prospectus. It should be filed with the relevant securities commissions in 40 days. The offering is expected to close in about 75 days. The company has a July 31 year-end. It is now September 8, Year 8.

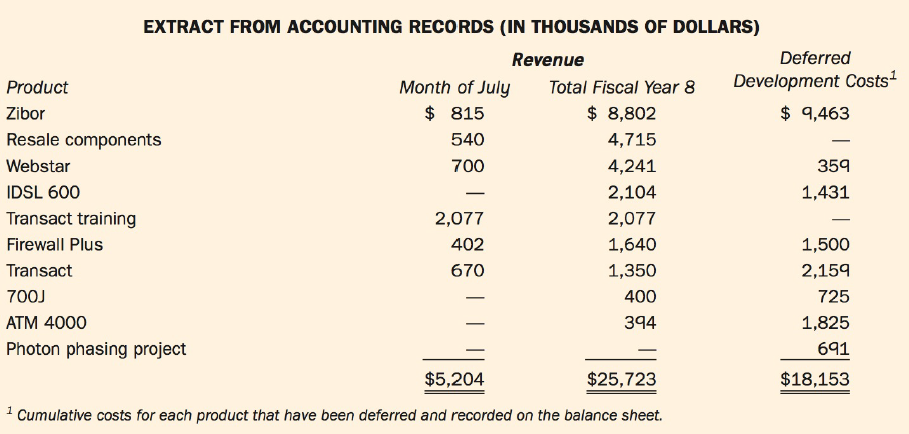

You, a CPA, work for Chesther Chathan, Chartered Professional Accountants, the auditors of ZIM since its inception. You have just been put in charge of ZIM's audit, due to the sudden illness of the senior. ZIM's year-end audit has just commenced. At the same time, ZIM's staff and the underwriters are working 15-hour days trying to write the prospectus, complete the required legal work, and prepare for the public offering. The client says that the audit must be completed so that the financial statements can go to the printer in 22 days. ZIM plans to hire a qualified chief financial officer as soon as possible. An extract from ZIM's accounting records is found in Exhibit IV. You have gathered the information in Exhibit V from the client. You have been asked by the audit partner to prepare a memo dealing with the key accounting issues.

Exhibit IV:

Exhibit V:

INFORMATION GATHERED FROM THE CLIENT

1. The job market for top software and hardware engineering talent is very tight. As a result, ZIM has turned to information technology "head hunters" to attract key personnel from other high-technology companies. During the year, ZIM paid $178,000 in placement fees, and the company is amortizing the payments over five years. The search firm offers a one-year money-back guarantee if any of the people hired leaves the company or proves to be unsatisfactory.

2. On July 29, Year 8, the company made a payment of $100,000 to a computer hacker. The hacker had given the company 10 days to pay her the funds. Otherwise, she said she would post on the Internet a security f law she had detected in the ZIM's Firewall Plus software.

3. Ale Zimmer had been working on a photon-phasing project when he left the telephone company . He has moved this technology ahead significantly at ZIM, and a prototype has been built at a cost of $691,000. The project has been delayed pending a decision on the direction that the project wi ll take.

4. ZIM defers and amortizes software and other development costs according to the fol lowing formula:

Annual amortization rate = sales in units for the, year/Total expected sales in units during product life

5. In line with normal software company practice, ZIM releases, via the Internet, software upgrades that correct certain bugs in previously released software.

6. During a routine visit to the AC&C Advanced Telecommunications laboratory in southern California, a ZIM engineer discovered that nearly 600 lines of code in an AC&C program were identical to those of some ZIM software written in Year 6-right down to two spelling mistakes and a programming error.

7. The ATM 4000 has been the company's only product flop. High rates of field failures and customer dissatisfaction led ZIM to issue an offer, dated July 30, Year 8, to buy back all units currently in service for a total of $467,500. Southwestern Utah Telephone is suing ZIM for $4 million for damages related to two ATM 4000 devices that it had purchased through a distributor. The devices broke down, affecting telephone traffic for two weeks before they were replaced.

8. ZIM also resells components manufactured by a Japanese telecommunications company . The effort required to make these sales to existing customers is minimal, but the gross margin is only 12% versus an average of 60% for the company's other products, excluding the Transact and 700J lines.

9. During the first two years of operation, ZIM expensed all desktop computers (PCs) when purchased, on the grounds that they become obsolete so fast that their value after one year is almost negligible. In the current year, ZIM bought $429,ooo worth of PCs and plans to write them off over two years.

10. Revenue is recognized on shipment for all equipment sold. Terms are FOB ZIM's shipping location.

11. ZIM's director of marketing, Albert Buzzer, has come up with a novel method of maximizing profits on the Transact product line. Transact is one of the few ZIM products that has direct competition. Transact routes telephone calls 20% faster than competing products but sells for 30% less. ZIM actually sells the product at a loss. However, without a special training course offered by ZIM, field efficiency cannot be maximized. Customers usually realize that they need the special training a couple of months after purchase. Buzzer estimates that the average telephone company will spend three dollars on training for every dollar spent on the product. Because of the way telephone companies budget and account for capital and training expenditures, most will not realize that they are spending three times as much on training as on the product.

12. In May Year 2, ZIM paid back a U.S. denominated, $25 million long-term debt prematurely to take advantage of a favourable interest rate. The US$25 million loan was subject to a cross-currency swap. The agreement with the third party was to pay CAN$33 million and receive US$25 million from the third party in May Year 4. This represented the exchange rate at the time the transactions were entered into. Although the swap was used to hedge the currency risk on the long-term debt, it was not formally designated as a hedge for reporting purposes. The U.S. dollars exchange rate at the time of the payout was CAN$1.20. ZIM recognized the $3 million gain on the repayment of the U.S. loan . ZIM negotiated a CAN$30 million one-year loan with Beemow Bank to repay the US$25 million loan . The spot exchange rate as at January 31, Year 3, was CAN$1.27, whereas the forward exchange rate for contracts expiring in May Year 4 was CAN$1.25.

13. The IDSL equipment was sold to customers in May Year 8. In September Year, ZIM provided the custom software required to operate the IDSL 600 equipment. The software was "shipped" via the Internet.

Financial StatementsFinancial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial... Exchange Rate

The value of one currency for the purpose of conversion to another. Exchange Rate means on any day, for purposes of determining the Dollar Equivalent of any currency other than Dollars, the rate at which such currency may be exchanged into Dollars...

Step by Step Answer:

Memo to Partner From CPA Re ZIM Inc Audit Overview There are a number of significant new issues pertaining to this years ZIM engagement particularly the pending initial public offering IPOFinancial st...View the full answer

Modern Advanced Accounting in Canada

ISBN: 978-1259087554

8th edition

Authors: Hilton Murray, Herauf Darrell