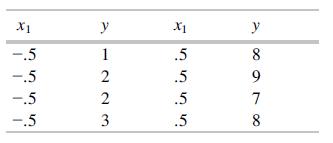

Question: Consider the model Y = 0 + 1 x 1 + for the following data: a. Determine the X and y matrices

Consider the model Y = β0 + β1x1 + ε for the following data:

a. Determine the X and y matrices and express the normal equations in terms of matrices.

b. Determine the β̂ vector, which contains the estimates for the two coefficients in the model.

c. Determine ŷ and e.

d. Calculate SSE (by summing the squared residuals) and then the estimated variance MSE.

e. Use MSE and (X'X)–1 to construct a 95% confidence interval for β1.

f. Carry out a t test of H0: β1 = 0 against a two-sided alternative.

g. Carry out the F test of H0: β1 = 0. How is this related to part (f)?

Ix y Tx 816 1223 7777

Step by Step Solution

3.52 Rating (162 Votes )

There are 3 Steps involved in it

Given the model Y 0 1x1 and the data set lets perform the necessary steps to solve the question a To determine the X and y matrices for the normal equ... View full answer

Get step-by-step solutions from verified subject matter experts