Question: Consider the following stochastic programming model: subject to The parameters a 2 and a 3 are independent and normally distributed random variables with means 5

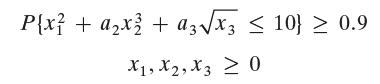

Consider the following stochastic programming model:![]()

subject to

The parameters a2 and a3 are independent and normally distributed random variables with means 5 and 2, and variance 16 and 25, respectively. Convert the problem into a (deterministic) separable programming form.

Maximize z = x + x + x3

Step by Step Solution

★★★★★

3.47 Rating (160 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Model Pxax s... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock