Question: Over the past 15 years, Anthonys Auto Shop has developed a reputation for reliable repairs and has grown from a one-person operation to a nine-person

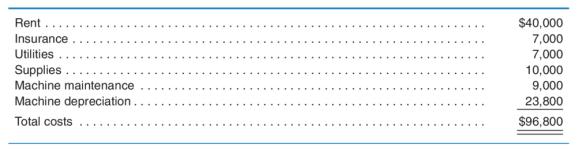

Over the past 15 years, Anthony’s Auto Shop has developed a reputation for reliable repairs and has grown from a one-person operation to a nine-person operation, including one manager and eight skilled auto mechanics. In recent years, however, competition from mass merchandisers has eroded business volume and profits, leading the owner, Anthony Axle, to ask his manager to take a closer look at the cost structure of the auto shop. The manager determined that direct materials (parts and components) are identified with individual jobs and charged directly to the customer. Direct labor (mechanics) is also identified with individual jobs and charged at a prespecified rate to the customers. The salary and benefits are $65,000 per year for a senior mechanic and $45,000 per year for a junior mechanic. Each mechanic can work up to 1,750 hours in a year on customer jobs, but if there are not enough jobs to keep all mechanics busy, the cost of their compensation still will have to be incurred. The manager’s salary and benefits amount to $75,000 per year. In addition, the following fixed costs are also incurred each year:

Because material costs are recovered directly from the customers, the profitability of the operation depends on the volume of business and the hourly rate charged for labor. At present, Anthony’s charges $51.06 per hour for all jobs. Anthony said he would not consider firing any of the four senior mechanics because he believes it is difficult to get workers with their skills and loyalty to the firm, but he is willing to consider releasing one or two of the junior mechanics.

The present job costing system uses a single conversion rate for all jobs. The cost driver rate is currently determined by dividing estimated total labor and overhead costs by expected hours charged to customers. The eight mechanics are expected to be busy on customer jobs for 95% of the total available time. The price of $51.06 per hour is determined by adding a markup of x% to the cost driver rate, that is $51.06 = [1 + x/100] × cost driver rate. Note that all personnel costs are included in conversion costs at present.

The manager is considering switching to the use of two rates, one for class A repairs and another for class B repairs. Electronic ignition system repairs and internal carburetor repairs are examples of class A repairs. Class A repairs require careful measurements and adjustments with equipment such as an oscilloscope or infrared gas analyzer. Class B repairs are simple repairs, such as shock absorber replacements and exhaust part replacements. Class A repairs can be done only by senior mechanics; class B repairs are done mainly by junior mechanics. Half the hours charged to customers are expected to be for class A repairs and half for class B repairs. Because class A repairs are expected to account for all of the senior mechanics’ time and most of the machine usage, 60% of the total costs (including personnel costs) are attributable to class A repairs and the remaining 40% to class B repairs.

Required

(a) Determine the markup of x% currently used.

(b) Determine the two new rates, one for class A repairs and one for class B repairs, using the same markup of x% that you determined in part (a).

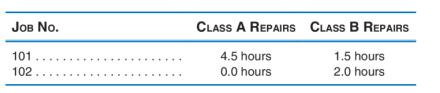

(c) The following are expected labor hours anticipated for two customer jobs:

Determine the price (in addition to materials) to be charged for each of the two jobs under the present accounting system and under the proposed accounting system.

(d) What change in service mix is likely to result from the proposed price change?

(e) Provide reasons why Anthony might retain the current costing system or change to the proposed costing system

Rent Insurance Utilities Supplies. Machine maintenance Machine depreciation.. Total costs $40,000 7,000 7,000 10,000 9,000 23,800 $96,800

Step by Step Solution

3.39 Rating (174 Votes )

There are 3 Steps involved in it

a To determine the markup currently used we need to find the cost driver rate Total estimated labor costs 65000 x 4 45000 x 4 440000 Total estimated o... View full answer

Get step-by-step solutions from verified subject matter experts