Based on Exhibit A and the mean of each of the valuation ratios, Logans estimate of Durtechs

Question:

Based on Exhibit A and the mean of each of the valuation ratios, Logan’s estimate of Durtech’s value per share should be closest to:

A. \($30.44\).

B. \($33.67\).

C. \($34.67\).

Josh Logan is a buy-side equity analyst who follows Durtech. Logan’s supervisor believes that Durtech is a likely takeover candidate and has asked Logan to estimate the company’s value per share in the event of an “all stock” takeover bid. Logan plans to estimate Durtech’s value per share using three approaches: discounted cash flow, comparable company analysis, and comparable transaction analysis.

Durtech has 1.2 million common shares outstanding and no outstanding long-term debt or preferred stock. Logan estimates that Durtech’s free cash flows at the end of the next three years will be \($5.0\) million, \($6.0\) million, and \($7.0\) million, respectively. After Year 3, he projects that free cash flow will grow at five percent per year. He determines the appropriate discount rate for this free cash flow stream is 15 percent per year.

Applying discounted cash flow analysis to the preceding information, Logan determines that Durtech’s fair enterprise value is \($61.8\) million. In a separate analysis based on ratios, Logan estimates that at the end of the third year, Durtech will be worth ten times its yearthree free cash flow.

Logan’s supervisor is troubled by the sensitivity of his enterprise value calculation to the terminal growth rate assumption. She asks Logan:

“What is the percentage change in your fair enterprise value of \($61.8\) million if you use a terminal growth rate of zero percent rather than five percent?”

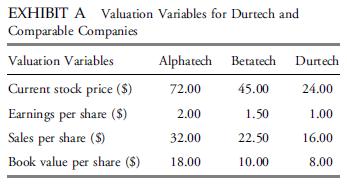

Logan gathers data on two companies comparable to Durtech: Alphatech and Betatech.

He believes that price-to-earnings, price-to-sales, and price-to-book-value per share of these companies should be used to value Durtech. The relevant data for the three companies are given in Exhibit A.

Logan also identifies one recent takeover transaction and analyzes its takeover premium (the amount by which its takeover price per share exceeds its current stock price). Omegatech is comparable to the possible transaction on Durtech. Omegatech had a stock price of \($44.40\) per share prior to a newspaper report of a takeover rumor. After the takeover rumor was reported, the price rose immediately to \($60.30\) per share. Eventually, the takeover offer was accepted by Omegatech’s shareholders for \($55.00\) per share. One-year trailing earnings per share for Omegatech immediately prior to the takeover were \($1.25\) per share.

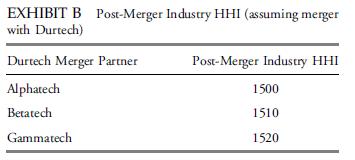

In order to evaluate the risk of government antitrust action, Logan computes the Herfindahl–Hirschman Index (HHI) for the industry group that includes Durtech.

He computes the pre-merger value of the HHI to be 1400. As shown in Exhibit B, Logan also computes the post-merger industry HHI assuming three possible merger scenarios with Durtech.

Based on this analysis, Logan concludes that the industry is moderately concentrated and that a merger of Durtech (with any of the companies listed in Exhibit B) will face a possible government challenge.

Step by Step Answer:

Corporate Finance A Practical Approach

ISBN: 9781118217290

2nd Edition

Authors: Michelle R Clayman, Martin S Fridson, George H Troughton, Matthew Scanlan