Consider the IBM call and put options in Problem 3. Ignoring any interest you might earn over

Question:

Consider the IBM call and put options in Problem 3. Ignoring any interest you might earn over the remaining few days’ life of the options:

a. Compute the break-even IBM stock price for each option (i.e., the stock price at which your total profit from buying and then exercising the option would be zero).

b. Which call option is most likely to have a return of −100%?

c. If IBM’s stock price is $131 on the expiration day, which option will have the highest return?

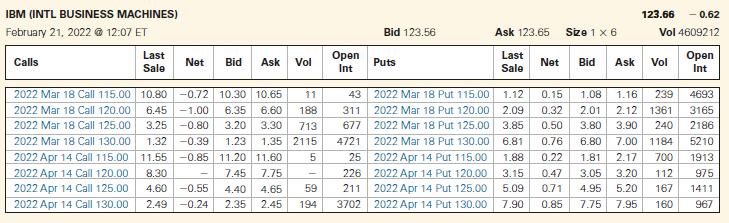

Data from in problem 3

Below is an option quote on IBM from the CBOE Web site showing options expiring in March and April 2022.

a. Which option contract had the most trades on that day?

b. Which option contract is being held the most overall?

c. Suppose you purchase one March 125 Call option. How much will you need to pay your broker for the option (ignoring commissions)?

d. Explain why the last sale price is not always between the bid and ask prices.

e. Suppose you sell one March 125 Put option. How much will you receive for the option (ignoring commissions)?

f. The calls with which strike prices are currently in-the-money? Which puts are in-the-money?

g. What is the difference between the March 115 Call option and the April 115 Call option?

Why is the second option more valuable?

h. On what date does the March 115 Call option expire? In what range must IBM’s stock price be at expiration for this option to be valuable?

Step by Step Answer:

To address your questions a b and c well need to use the options pricing information provided The questions refer to computing breakeven prices evaluating which option is most likely to have a return ...View the full answer