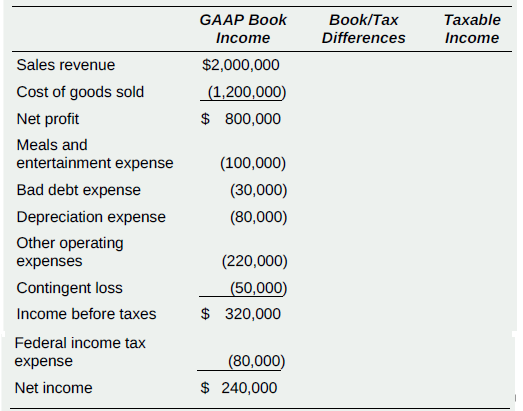

Grim Corporation has income and expenses for its current fiscal year, recorded under generally accepted accounting principles,

Question:

Grim Corporation has income and expenses for its current fiscal year, recorded under generally accepted accounting principles, as shown in the following schedule. In addition, a review of Grim’s books and records reveals the following information:

- Grim expensed, for book purposes, meals totaling $46,000 and entertainment costs totaling $54,000. These costs were incurred by Grim sales personnel, are reasonable in amount, and are documented in company records.

- During January of the current year, Grim was sued by one of its employees as a result of a work-related accident. The suit has not yet gone to court. However, Grim’s auditors required the company to record a contingent liability (and related book expense) for $50,000, reflecting the company’s likely liability from the suit.

- Grim recorded federal income tax expense for book purposes of$80,000.

- Grim used the reserve method for calculating bad debt expenses for book purposes. Its book income statement reflects bad debt expense of $30,000, calculated as 1.5 percent of sales revenue. Actual write offs of accounts receivable during the year totaled $22,000.

- MACRS depreciation for the year totals $95,000.

a. Complete the following table, reflecting Grim’s book/tax differences for the current year, whether such differences are positive (increase taxable income) or negative (decrease taxable income), and the final numbers to be included in the calculation of taxable income on Grim’s tax return.

b. Prepare a Schedule M-1, page 5, Form 1120, reconciling Grim’s book and taxable income.

Accounts receivables are debts owed to your company, usually from sales on credit. Accounts receivable is business asset, the sum of the money owed to you by customers who haven’t paid.The standard procedure in business-to-business sales is that... Corporation

A Corporation is a legal form of business that is separate from its owner. In other words, a corporation is a business or organization formed by a group of people, and its right and liabilities separate from those of the individuals involved. It may...

Step by Step Answer:

a b Schedule M1 Sales revenue Cost of goods sold Net profit Meals and entertainm...View the full answer

Principles Of Taxation For Business And Investment Planning 2019 Edition

ISBN: 9781260161472

22nd Edition

Authors: Sally Jones, Shelley C. Rhoades Catanach, Sandra R Callaghan