Handy Distributors Inc. (HDI) includes a wholesale division and a retail division. Relevant information pertaining to its

Question:

Handy Distributors Inc. (HDI) includes a wholesale division and a retail division. Relevant information pertaining to its retail division (RET) is as follows:

- The net assets of RET were acquired by HDI in 20X1. HDI allocated $400,000 to goodwill upon acquisition.

- RET is a cash-generating unit (CGU). Its assets have not previously been impaired.

- HDI reports its financial results in accordance with !FRS.

- HDI's year end is December 31.

- RET uses the cost model to subsequently measure its plant and equipment and the revaluation model to subsequently measure its land. It transfers the revaluation surplus, if any, to retained earnings only upon derecognition.

- RET depreciates all assets annually. It depreciates its buildings using the straight-line method and its equipment using the double-declining balance method.

Part A;

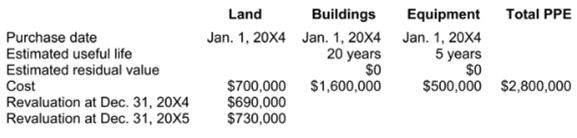

Details of the cost and revaluation values of the PPE follow:

Required:

(a) Calculate the annual depreciation of each asset held by RET for each of the 20X4 and 20X5 fiscal years.

(b) Provide the year-end adjusting journal entries pertaining to the revaluation of the land and depreciation on the other assets for the 20X4 and 20X5 fiscal years. Ensure that the journal entries are dated and include a brief description of the pertinent details. Prepare a separate journal entry pertaining to each asset class. Supporting calculations are to be referenced or included in the description.

Part B:

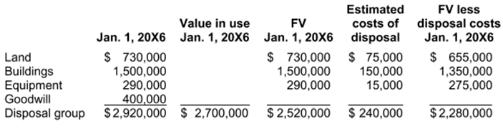

On January 1, 20X6, the Board of Directors of HDI decided to list the CGU, RET, for sale and determined that it met the criteria of a disposal group. Independent of Part A. assume that RET had previously used the cost model to value its PPE. Following is the net book value of the various assets, together with their estimated fair value and other information:

- HDI estimates that the value in use of the RET disposal group is $2,700,000.

- HDI estimates that the fair value of the RET disposal group is $2,520,000 and that the disposal costs will be approximately $240,000. Note that the fair value of a disposal group can be greater than the fair value of the individual assets.

On June 14, 20X6, HDI received $2,385,000 cash from the sale of the RET disposal group ($2,660,000 less a $275,000 sales commission).

Required:

Prepare a summary of the journal entries RET will need to make to record the board's decision to designate RET as a disposal group and to record its subsequent sale. Ensure that the journal entries are dated and include a brief description of the pertinent details. Supporting calculations are to be referenced or included in the description of each journal entry.

Expert Answer:

Part A a Annual depreciation LAND BUILDINGS EQUIPMENT estimated useful life 20 years 5 years cost 700000 1600000 500000 estimated residual value 0 0 Annual depreciation Costresidual valueUseful life 8... View the full answer

Financial and Managerial Accounting the basis for business decisions

ISBN: 978-0078111044

16th edition

Authors: Jan Williams, Susan Haka, Mark Bettner, Joseph Carcello