Minnie Co. has an unfunded prepaid/accrued pension cost of $2,000 (debit balance) at December 31, 2010. The

Question:

Minnie Co. has an unfunded prepaid/accrued pension cost of $2,000 (debit balance) at December 31, 2010. The following information pertains to 2011:

Pension expense??????????????????....$320,000

Projected benefit obligation, December 31, 2011?????...840,000

Contributions???????????????????........330,000

Plan assets (fair value), December 31, 2011???????..810,000

Refer to Exhibit 20-2. The balance in Prepaid/Accrued Pension Cost at December 31, 2011, should be

a) $30,000 debit

b) $30,000 credit

c) $ 8,000 credit

d) $10,000 credit

2.Minnie Co. has an unfunded prepaid/accrued pension cost of $2,000 (debit balance) at December 31, 2010. The following information pertains to 2011:

Pension expense?????????????????....$320,000

Projected benefit obligation, December 31, 2011????...840,000

Contributions??????????????????........330,000

Plan assets (fair value), December 31, 2011??????..810,000

Other Comprehensive Income????????????....30,000

Accrued/Prepaid Pension Cost????????????...30,000

Accrued/Prepaid Pension Cost????????????...30,000

Other Comprehensive Income???????????? ...30,000

Other Comprehensive Income????????????....42,000

Accrued/Prepaid Pension Cost????...???????...42,000

Accrued/Prepaid Pension Cost???????????......40,000

Other Comprehensive Income????????????...40,000

3. The Margie Company has a defined benefit pension plan for its employees. The following information pertains to the pension plan as of December 31, 2010:

Projected benefit obligation, January 1, 2010????$1,600,000

Service cost, 2010????????????????...750,000

Interest cost, 2010????????????????...100,000

Payments to retired employees?????????..........80,000

Actual return on plan assets?????????...............99,600

a) $2,250,000

b) $2,270,400

c) $2,370,000

d) $2,450,000

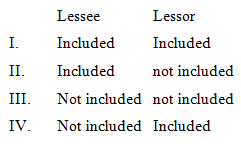

4. According to current GAAP, leased property recorded as a capital lease normally should be reported as a long-term or intangible asset on the balance sheet of the lessee and the lessor as follows:

5. On January 1, 2010, Leslie Company signed a lease agreement requiring ten annual payments of $14,000, beginning December 31, 2010. The agreement was classified as a capital lease. When reviewing Leslie's accounting records, which of the following would not be expected?

Leased Equipment???????????????.105,210

Capital Lease Obligation????????????..105,210

Interest Expense?????????????????7,365

Obligation under Capital Leases???????.....?...6,635

Cash????????????????????..?14,000

Depreciation Expense: Leased Equipment???..?..10,521

Accumulated Depreciation:

Leased Equipment??????????????....10,521

Rent Expense????????????????...14,000

Cash????????????????????....14,000

6. On January 1, 2010, Wally Company signed a four-year lease requiring annual payments of $45,000, with the first payment due on January 1, 2010. Wally's incremental borrowing rate was 6%. Actuarial information for 6% follows:

4 Periods

Present value of an annuity due of 1 @ 6%............................3.67301

Present value of ordinary annuity of 1 @ 6%..........................3.46511

Assuming the lease qualifies as a capital lease, what amount should be recorded as leased equipment under capital leases on January 1, 2010 (rounded to the nearest dollar)?

a) $200,931

b) $165,285

c) $155,931

d) $144,555

7. On January 1, 2010, Rayma Co. leased equipment by signing a six-year lease that required six payments of $30,000 due on January 1 of each year with the first payment due January 1, 2010. The equipment remains the property of the lessor at the end of the lease, and Rayma does not guarantee any residual value. Using an 8% cost of capital, Rayma capitalized the lease on January 1, 2010, in the amount of $149,781. What is the total amount of lease liability (including interest) Rayma should report as of December 31, 2011?

a) $99,364

b) $107,313

c) $119,781

d) 121,415

8. A capital lease should be recorded in the lessee's accounts at the inception of the lease in an amount equal to

a) The present value of the minimum lease payments less the executory costs included in the minimum lease payments

b) The total value of the future rental payments less any estimated contingent payments

c) The total value of future rental payments less any executory payments included in the future payments

d) The total value of the minimum lease payments less executory costs, if any

Expert Answer: