Scofield Enterprises has been operating for one year and the company needs additional working capital to expand

Question:

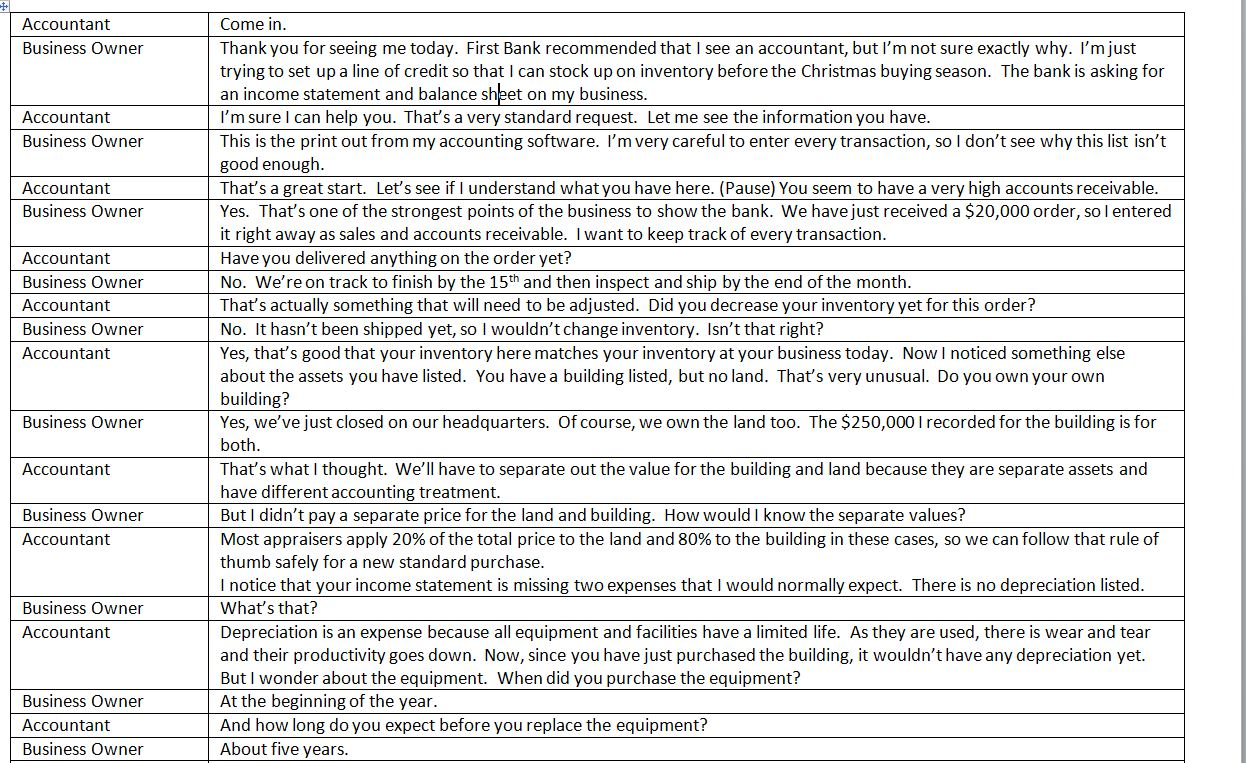

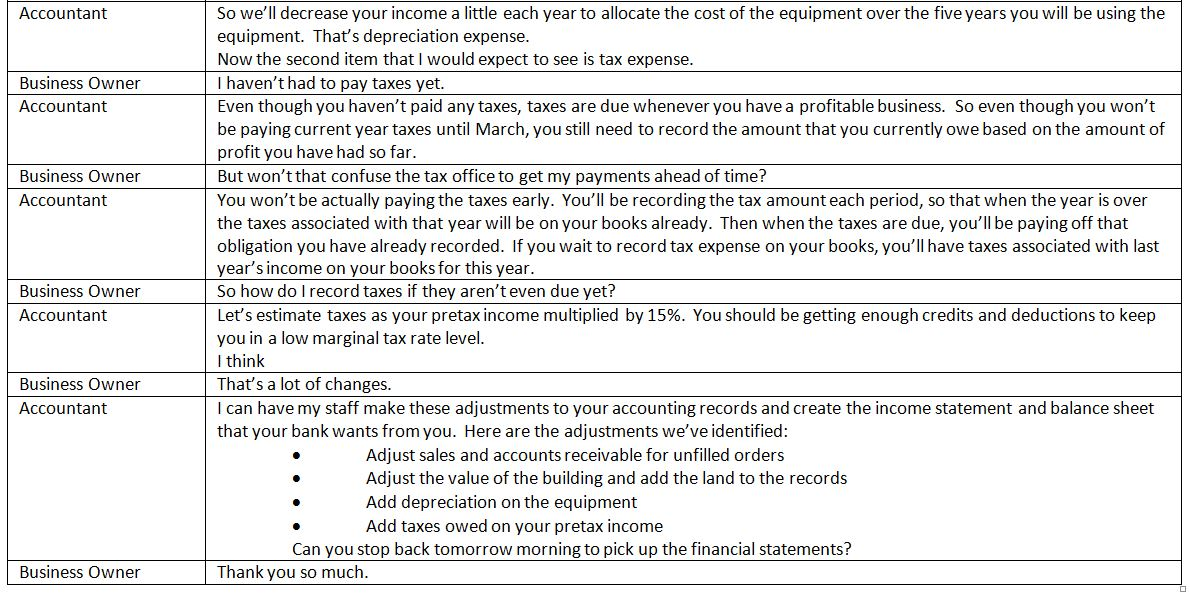

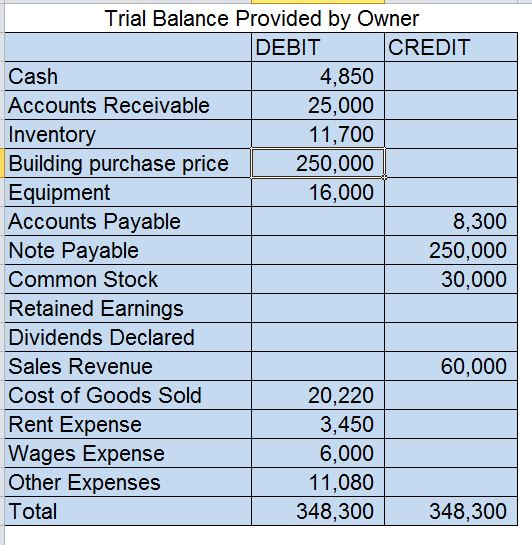

Scofield Enterprises has been operating for one year and the company needs additional working capital to expand its business. The owner doesn't really know whether the business is profitable or not, but she is sure from the increase in orders already experienced that the business concept can be successful. Now she needs to provide GAAP-compliant financial statements to the banker and may hire your company to create them. The company has been entering information in general ledger software all year and the software has generated an Unadjusted Trial Balance which is available separately in a spreadsheet. The owner of Scofield Enterprises sat down with your boss this week when she realized that the bank wasn't going to accept the computer output, and their conversation is available at ACCT 3310 Professional Application: Part I provided below in this folder.

Listen to and watch the conversation between the accountant and the owner at ACCT 3310 - Professional Application: Part I. Use the unadjusted trial balance on the Original Trial Balance worksheet, plus the information you gather from the owner / accountant's discussion to develop GAAP-compliant financial statements Prepare adjusting / error correction journal entries in the General Journal worksheet. Prepare an Adjusted Trial Balance on the Trial Balance worksheet. Prepare an Income Statement, Statement of Retained Earnings, and Balance Sheet Prepare a memorandum in a separate WORD file to the owner that presents your evaluation of the company's cash management and profitability and explains the transformation of the unadjusted trial balance to finished financial statements.

Expert Answer:

Intermediate Accounting

ISBN: 978-0324592375

17th Edition

Authors: James D. Stice, Earl K. Stice, Fred Skousen