The functional currency of Bertrand, Inc.'s Irish subsidiary is the euro. Bertrand borrowed euros as a partial

Question:

The functional currency of Bertrand, Inc.'s Irish subsidiary is the euro. Bertrand borrowed euros as a partial hedge of its investment in the subsidiary. Since then, the euro has decreased in value. Bertrand's negative translation adjustment on its investment in the subsidiary exceeded its foreign exchange gain on its euro borrowing. How should Bertrand report the effects of the negative translation adjustment and foreign exchange gain in its consolidated financial statements?

a. Report the translation adjustment in accumulated other comprehensive income on the balance sheet and the foreign exchange gain as a gain on the income statement. b. Report the translation adjustment in the income statement and defer the foreign exchange gain in accumulated other comprehensive income on the balance sheet.

c. Report the translation adjustment less the foreign exchange gain in accumulated other comprehensive income on the balance sheet.

d. Report the translation adjustment less the foreign exchange gain in the income statement.

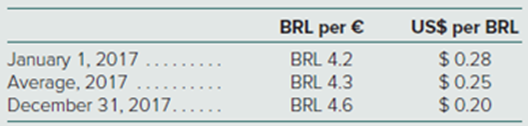

Problems 20 and 21 are based on the following information.

McCarthy, Inc.'s Brazilian subsidiary borrowed 100,000 euros on January 1, 2017. Exchange rates between the Brazilian real (BRL) and euro (?) and between the U.S. dollar ($) and BRL are as follows:

Expert Answer:

International Accounting

ISBN: 978-1260466539

5th edition

Authors: Timothy Doupnik, Mark Finn, Giorgio Gotti, Hector Perera