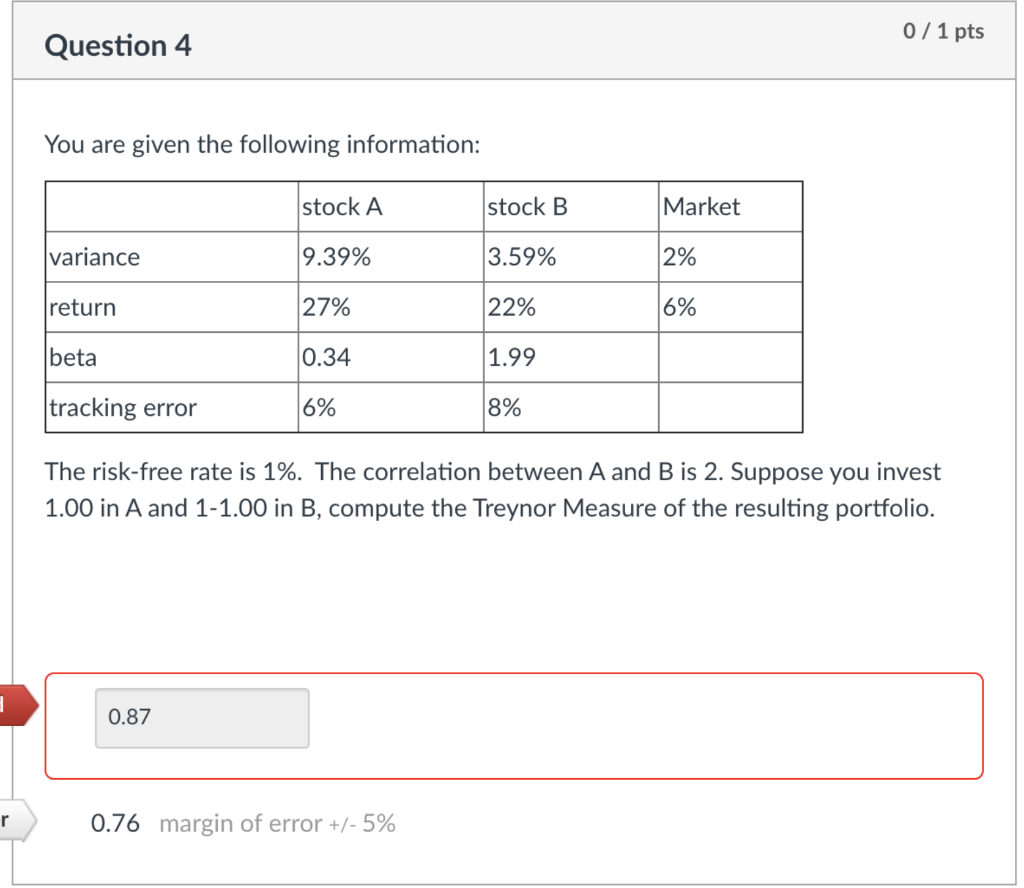

Question: 0 / 1 pts Question 4 You are given the following information: stock A stock B Market variance 9.39% 3.59% 2% return 27% 22% 6%

0 / 1 pts Question 4 You are given the following information: stock A stock B Market variance 9.39% 3.59% 2% return 27% 22% 6% beta 0.34 1.99 tracking error 6% 8% The risk-free rate is 1%. The correlation between A and B is 2. Suppose you invest 1.00 in A and 1-1.00 in B, compute the Treynor Measure of the resulting portfolio. 0.87 r 0.76 margin of error +/- 5%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock