Question: 0 Some new software systems (e.g., software over inventory and trade receivables) were implemented across the year. However, the general ledger system has not yet

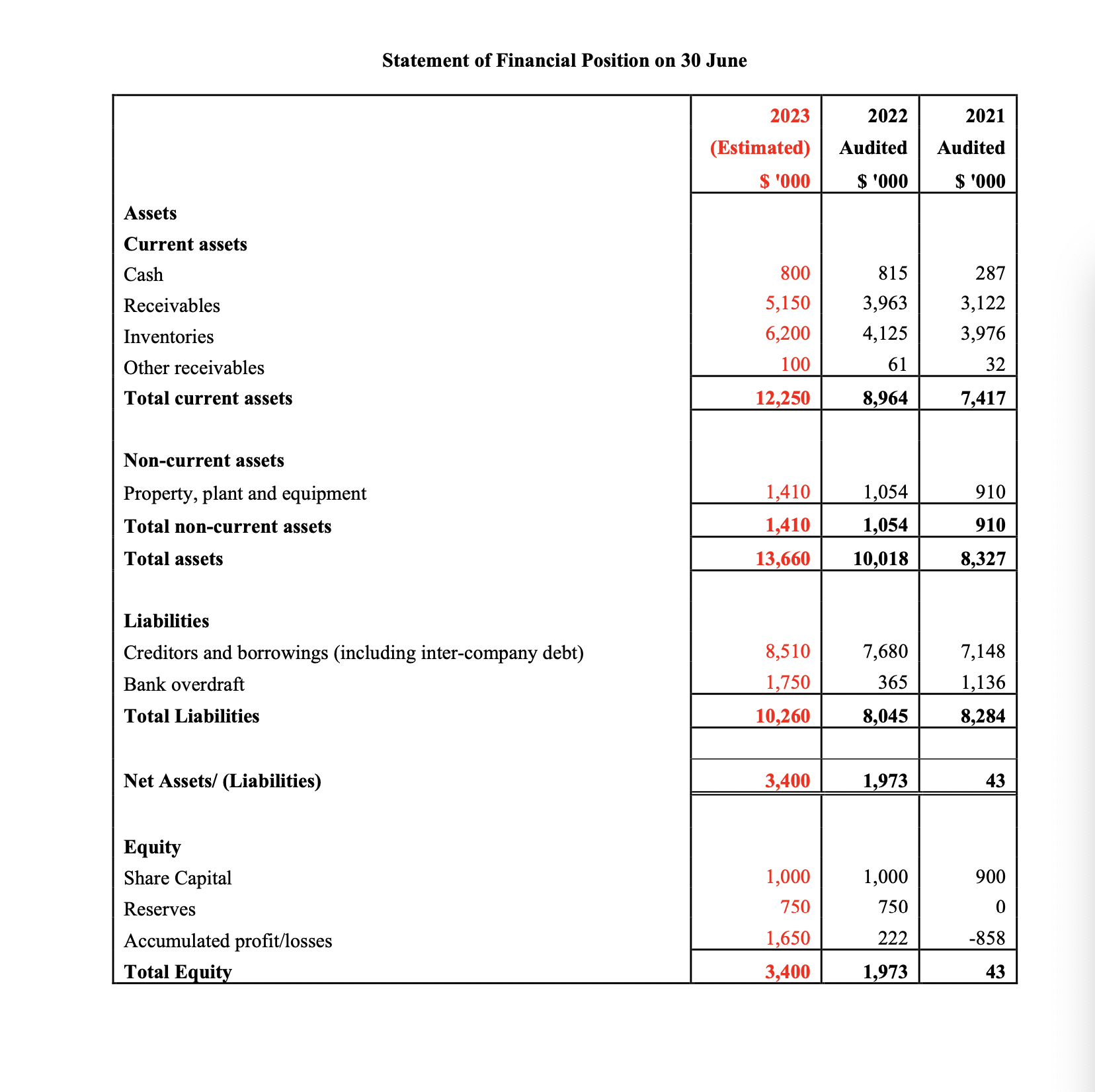

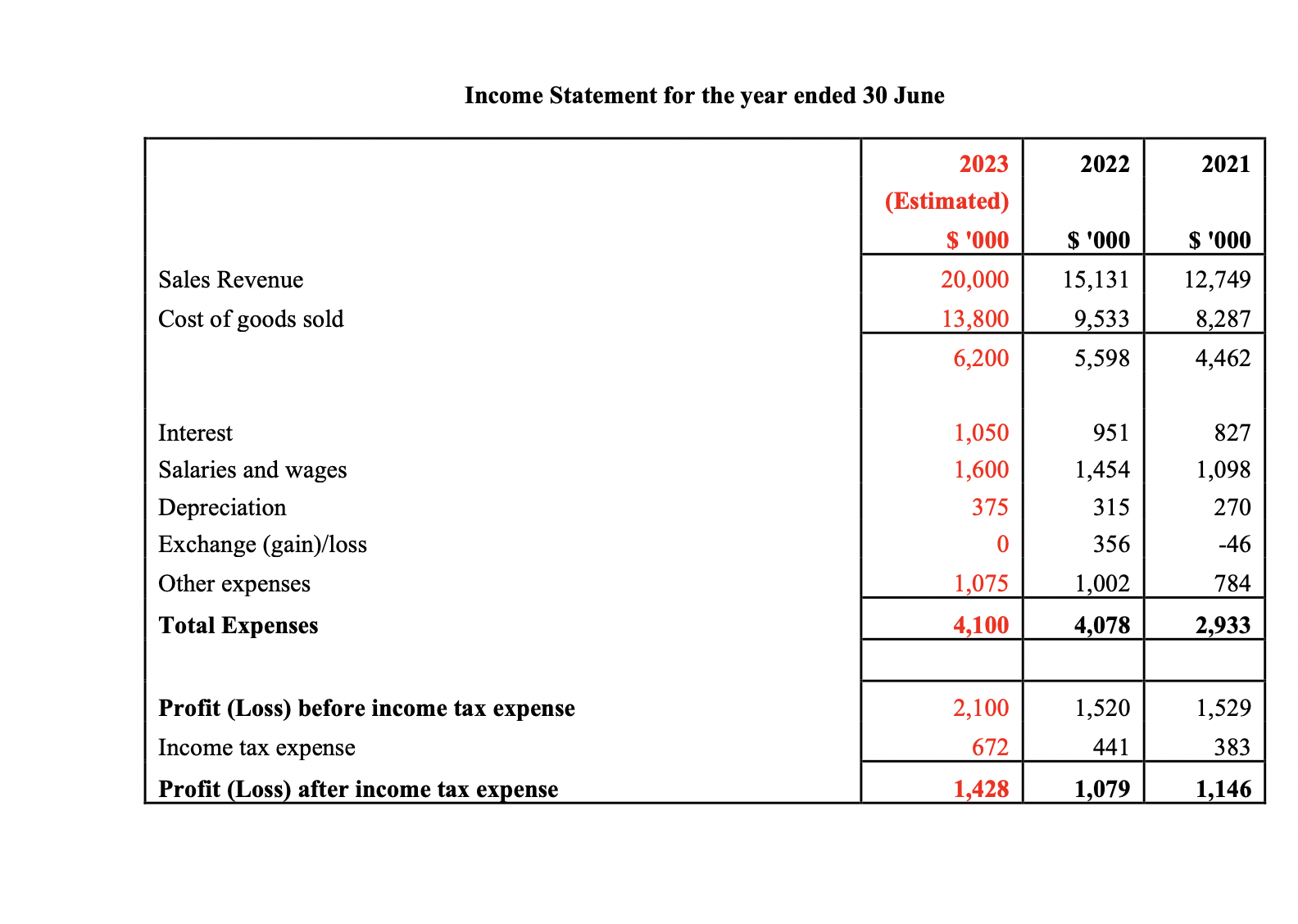

0 Some new software systems (e.g., software over inventory and trade receivables) were implemented across the year. However, the general ledger system has not yet been integrated with them. Reconciliations are carried out between the subsidiary ledgers and the general ledger control accounts on a monthly basis. During the process of reconciling the inventory account, the accounting manager identied some unknown mistakes, and he doubted that these mistakes were caused by the differences in exchange rates used when converting overseas purchases between the subsidiary and general ledgers. Last month's unreconciled difference was $234,000. 0 There will be no lll physical inventory count at the end of this year. This is because a cyclical stocktaking method was implemented earlier in the year, and auditors did not nd any issues with recording physical inventory. You were not aware of this until the planning meeting. 0 Some suppliers complained to the HQE sales team that they don't want to receive more conrmation requests (i.e., in 2022 audit). The sales manager has therefore requested that the auditors shall not contact some suppliers at the forthcoming year end (i.e., in 2023 audit). 0 The manager recently dismissed an employee because he was found to create false records of his working hours, resulting in overpayment to him. The overpayment was $14,000 (over a period of 7 months). You, as the audit senior, examined the payroll system during last year's audit, and did not look at this specic aspect of the system. The manager was angry that the auditor did not identify the weakness in the payroll system. The audited income statement and balance sheet for the last two years together with management's estimates for this year are as follows. a 1. L a 5. Perform an assessment of the ability of the company to continue as a going concern in the future. Justify your answer. 6. How would you answer the client's concern that you did not identify the problems in the payroll system or even advise them of the internal control weakness? Case Information: You are the audit senior of High-Quality Equipment Pty Limited (HQE), a consumer electronics and home appliances manufacturing company. Mobile Technology Pty Ltd (MT), a publicly listed company in the United States, is a mobile phone manufacturer. HQE is the wholly owned subsidiary of MT (i.e., MT is holding 100% shares of HQE). HQE was found in Australia in 2017. During the last ve years, HQE has been protable and the growth in revenue has been substantial. However, liquidity has been a major problem. To resolve this liquidity issue, HQE has chosen not to repay the debt owed to MT, and MT approved this request because it believes that HQE can become a \"cash cow\" in the 1ture. Due to the rapid growth of HQE, the company's staff and accounting systems were under pressure. For example, HQE employed many temporary staff in the accounting department to make sure they can process daily transactions on time. Meanwhile, projects aimed at keeping the accounting systems up to date with business growth are undertaken by full-time employees. The accounting department has experienced a signicant staff turnover in the past two years, which can be attributed to the demands of a rapidly expanding business, including high pressure and long working hours. HQE has 12 full-time employees in the accounting department. However, apart from the nancial controller and management accountant, no other employee has been with the company for more than two years. You are planning the 30 June 2023 year end audit of HQE and have recently had a planning meeting with the nancial controller. At this meeting you were informed of the following: I It is expected that the sales will be $20 million in 2023. The primary reason for the increase from the previous year is a signicant order received from the Victoria State Government." 0 Gross margin is expected to be 31%. The decline in margin can be attributed to challenges experienced during the year, resulting in a signicant quantity of products being air-freighted on short notice from the parent company. I From discussions with the credit manager, you realized that the accounts receivable is running at 93 days, which exceeds the industry norm of 70 days, while third-party creditors are typically paid within 45 days. 0 Inventory at the 2023 year-end is expected to be $6.2 million. Despite a decrease in the order book over the past few months, management made the decision to maintain production at its maximum capacity. In anticipation of a temporary decrease in orders (i.e., just a short-term but not a long-term trend), management chose not to terminate manufacturing staff. Also, it is expected that HQE will receive another big order from the Victoria State Government after the year end. Management aims to surpass delivery time expectations and achieve a competitive advantage over other companies. Statement of Financial Position on 30 June 2023 (Estimated) S '000 Assets Current assets Cash Receivables Inventories Other receivables Total current assets 12,250 8,964 Non-current assets Property, plant and equipment 1,410 1,054 910 Total non-current assets 1,410 1,054 910 Total assets 13,660 10,018 8,327 Liabilities Creditors and borrowings (including intercompany debt) 8,510 7,680 7,148 Bank overdraft 1,750 365 1,136 Total Liabilities 10,260 8,045 8,2 84 Net Assets] (Liabilities) 3,400 1,973 Equity Share Capital Reserves Accumulated prot/losses Totamui 3,400 Income Statement for the year ended 30 June 2023 2022 2021 $ '000 $ '000 $ '000 Cost of goods sold 13,800 9,533 8,287 Interest Salaries and wages Depreciation Exchange (gain)/loss Other expenses Total Expenses Prot (Loss) before income tax expense 2,100 1,520 1,529 Income tax expense 672 441 3 83 Prot Loss after income tax ex . ense 1,428 1,079 1,146

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!