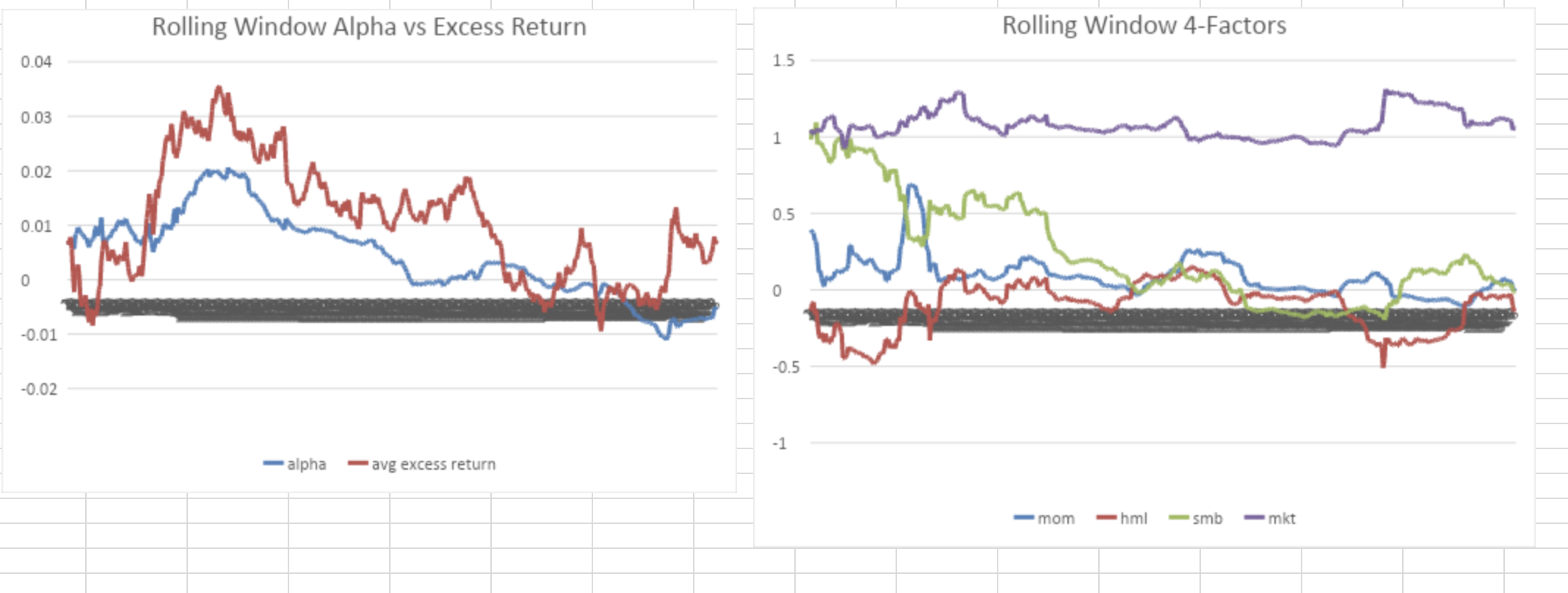

Question: 0.02 - alpha -avg excess return 1 3. Interpret the development of the coefficients with respect to the data provided about the fund (changes of

0.02 - alpha -avg excess return 1 3. Interpret the development of the coefficients with respect to the data provided about the fund (changes of the manager, expenses,...). Do you see any connection to the facts about the fund? Comment on the alphas. Hint: This is an open-ended question, i.e. there isn't one correct answer. It is sufficient to discuss a few things you notice about the relationship between the fund's betas and the other information you know about the fund. 0.02 - alpha -avg excess return 1 3. Interpret the development of the coefficients with respect to the data provided about the fund (changes of the manager, expenses,...). Do you see any connection to the facts about the fund? Comment on the alphas. Hint: This is an open-ended question, i.e. there isn't one correct answer. It is sufficient to discuss a few things you notice about the relationship between the fund's betas and the other information you know about the fund

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts