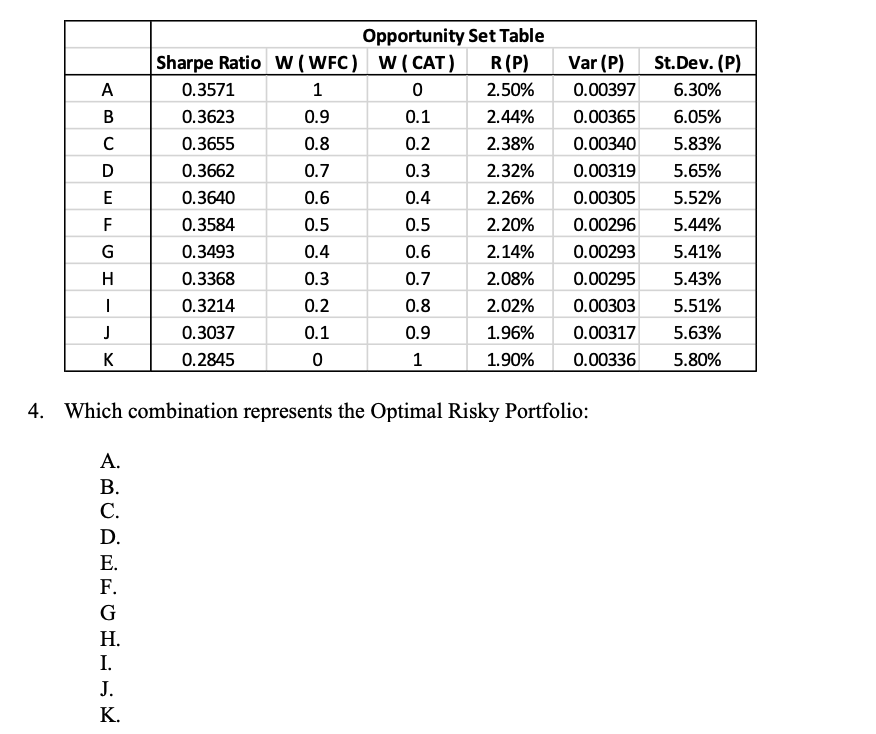

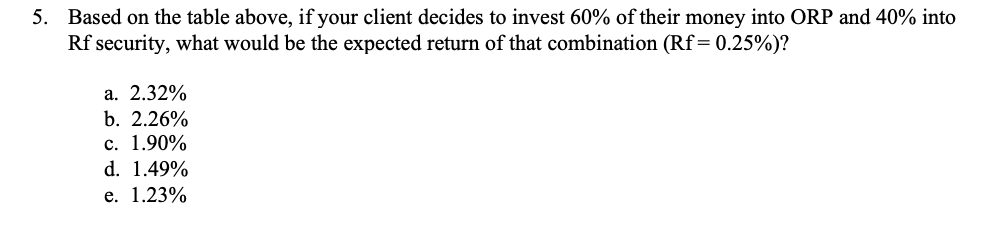

Question: 0.2 A B D E F G . 1 Opportunity Set Table Sharpe Ratio W (WFC) W (CAT) R(P) 0.3571 1 0 2.50% 0.3623 0.9

0.2 A B D E F G . 1 Opportunity Set Table Sharpe Ratio W (WFC) W (CAT) R(P) 0.3571 1 0 2.50% 0.3623 0.9 0.1 2.44% 0.3655 0.8 2.38% 0.3662 0.7 0.3 2.32% 0.3640 0.6 0.4 2.26% 0.3584 0.5 0.5 2.20% 0.3493 0.4 0.6 2.14% 0.3368 0.3 0.7 2.08% 0.3214 0.2 0.8 2.02% 0.3037 0.1 0.9 1.96% 0.2845 0 1 1.90% Var (P) 0.00397 0.00365 0.00340 0.00319 0.00305 0.00296 0.00293 0.00295 0.00303 0.00317 0.00336 St.Dev. (P) 6.30% 6.05% 5.83% 5.65% 5.52% 5.44% 5.41% 5.43% 5.51% 5.63% 5.80% J 4. Which combination represents the Optimal Risky Portfolio: B. C. D. E. F. G H. I. J. K. 5. Based on the table above, if your client decides to invest 60% of their money into ORP and 40% into Rf security, what would be the expected return of that combination (Rf= 0.25%)? a. 2.32% b. 2.26% c. 1.90% d. 1.49% e. 1.23%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts