Question: 1 1 . 2 9 . Consider a put option on a non - dividend - paying stock when the stock price is $ 4

Consider a put option on a nondividendpaying stock when the stock price is $ the strike price is $ the riskfree interest rate is the volatility is per annum, and the time to maturity is three months. Use DerivaGem to determine the following:

a The price of the option if it is European use BlackScholes: European

b The price of the option if it is American use Binomial: American with tree steps

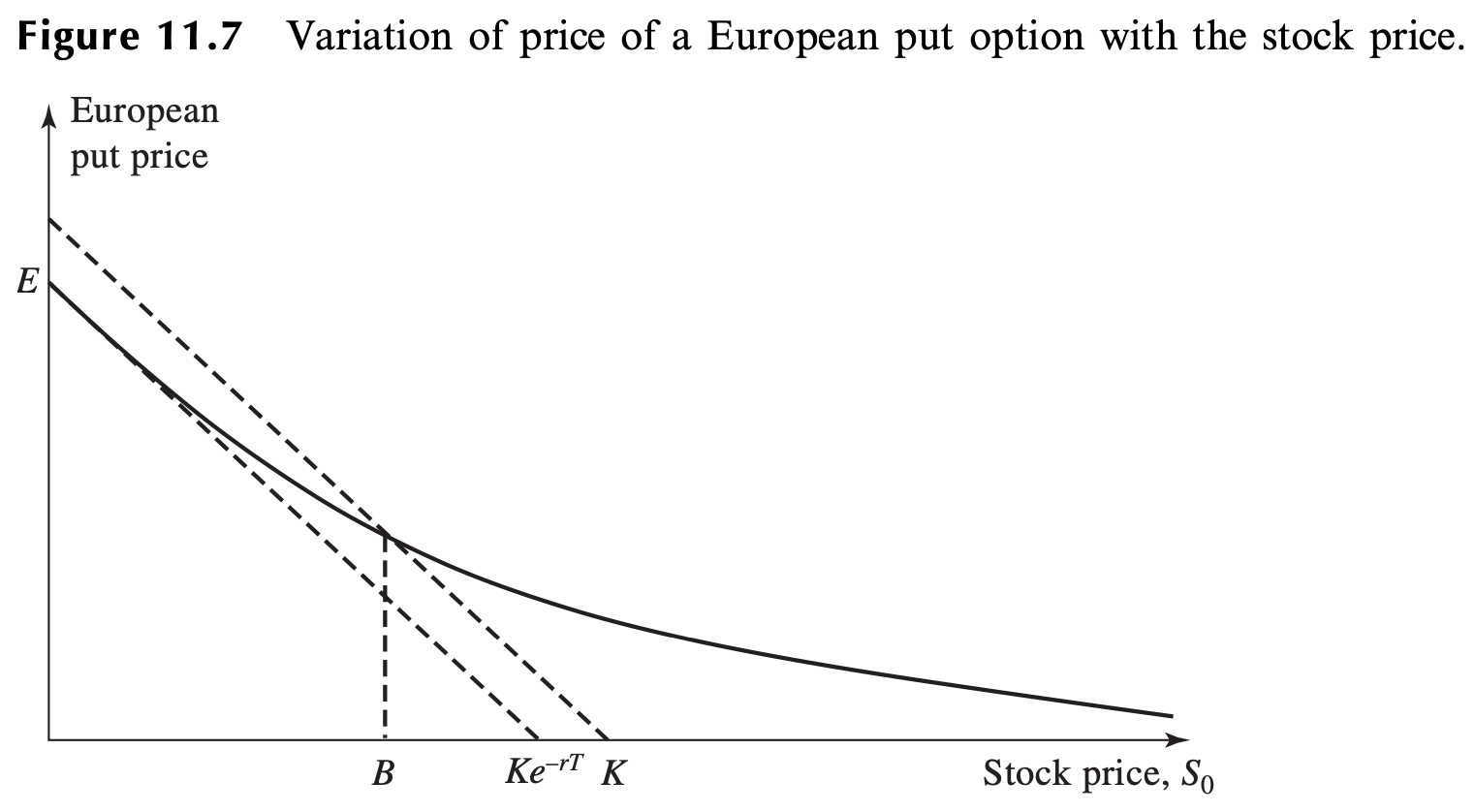

c Point B in Figure Figure Variation of price of a European put option with the stock price.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock