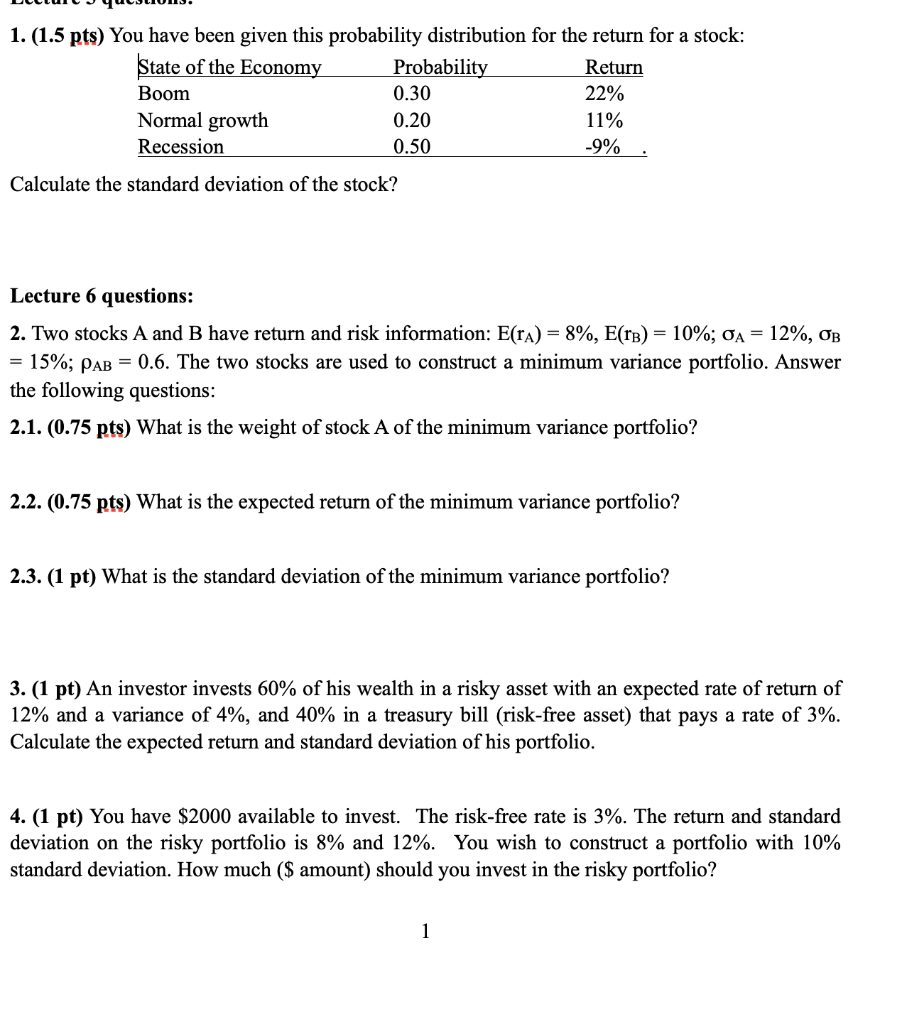

Question: 1. (1.5 pts) You have been given this probability distribution for the return for a stock: State of the Economy Probability 0.30 Return 22% Boom

1. (1.5 pts) You have been given this probability distribution for the return for a stock: State of the Economy Probability 0.30 Return 22% Boom Normal growth 0.20 11% Recession -9% 0.50 Calculate the standard deviation of the stock? Lecture 6 questions: 2. Two stocks A and B have return and risk information: E(rA) = 8%, E(rB) = 10%; oA = 12%, oB = 15%; pAB= 0.6. The two stocks are used to construct a minimum variance portfolio. Answer the following questions: 2.1. (0.75 pts) What is the weight of stock A of the minimum variance portfolio? 2.2. (0.75 pts) What is the expected return of the minimum variance portfolio? 2.3. (1 pt) What is the standard deviation of the minimum variance portfolio? 3. (1 pt) An investor invests 60% of his wealth in a risky asset with an expected rate of return of 12% and a variance of 4%, and 40% in a treasury bill (risk-free asset) that pays a rate of 3%. Calculate the expected return and standard deviation of his portfolio. 4. (1 pt) You have $2000 available to invest. The risk-free rate is 3%. The return and standard deviation on the risky portfolio is 8% and 12%. You wish to construct a portfolio with 10% standard deviation. How much ($ amount) should you invest in the risky portfolio? 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts