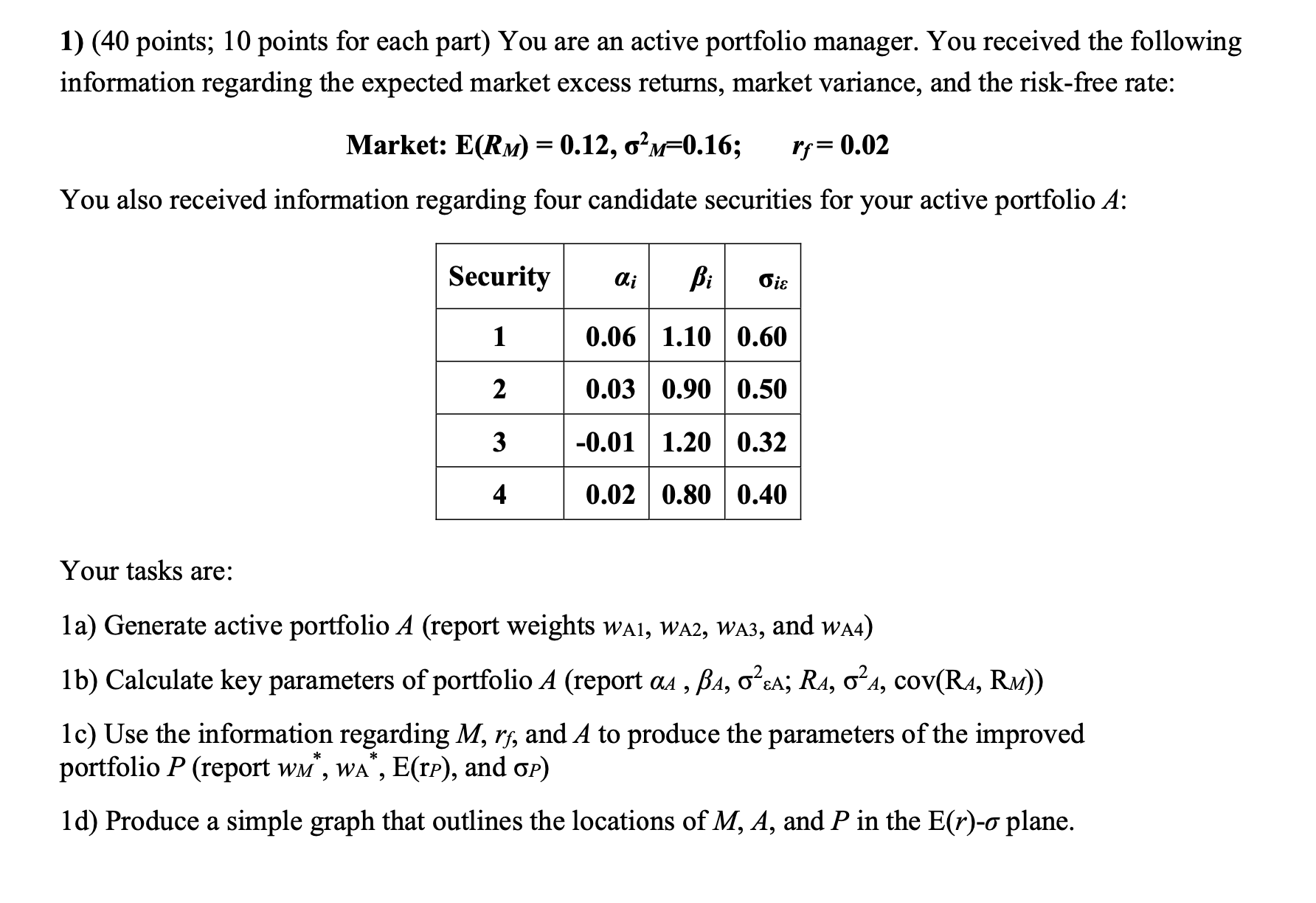

Question: 1) (40 points; 10 points for each part) You are an active portfolio manager. You received the following information regarding the expected market excess returns,

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock