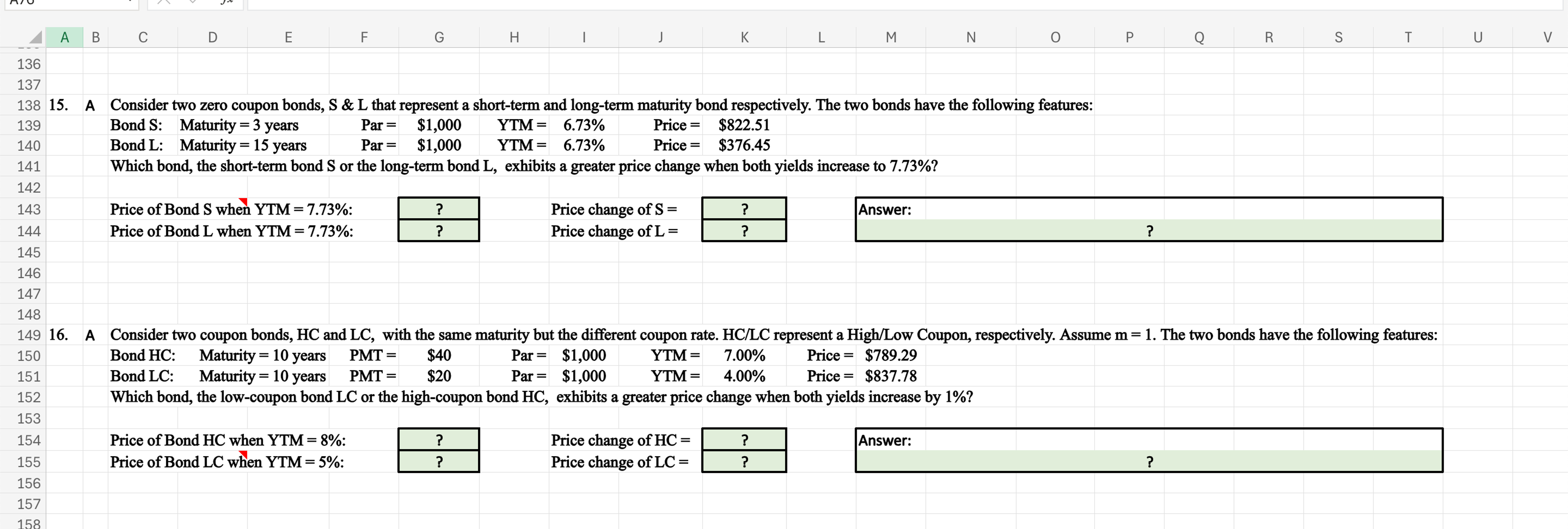

Question: 1 5 . A Consider two zero coupon bonds, S & L that represent a short - term and long - term maturity bond respectively.

A Consider two zero coupon bonds, & that represent a shortterm and longterm maturity bond respectively. The two bonds have the following features:

Bond : Maturity years $Par$ Price $

Bond LC: Maturity years $Par$ Price $

Which bond, the lowcoupon bond LC or the highcoupon bond HC exhibits a greater price change when both yields increase by

Price of Bond when :

Price change of

Price of Bond LC when :

Price change of

A Consider two coupon bonds, HC and LC with the same maturity but the different coupon rate. HCLC represent a HighLow Coupon, respectively. Assume m The two bonds have the following features:

Bond HC: Maturity years PMT $ Par $ YTM Price $

Bond LC: Maturity years PMT $ Par $ YTM Price $

Which bond, the lowcoupon bond LC or the highcoupon bond HC exhibits a greater price change when both yields increase by

Compute all in excel using excel formulas please

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock