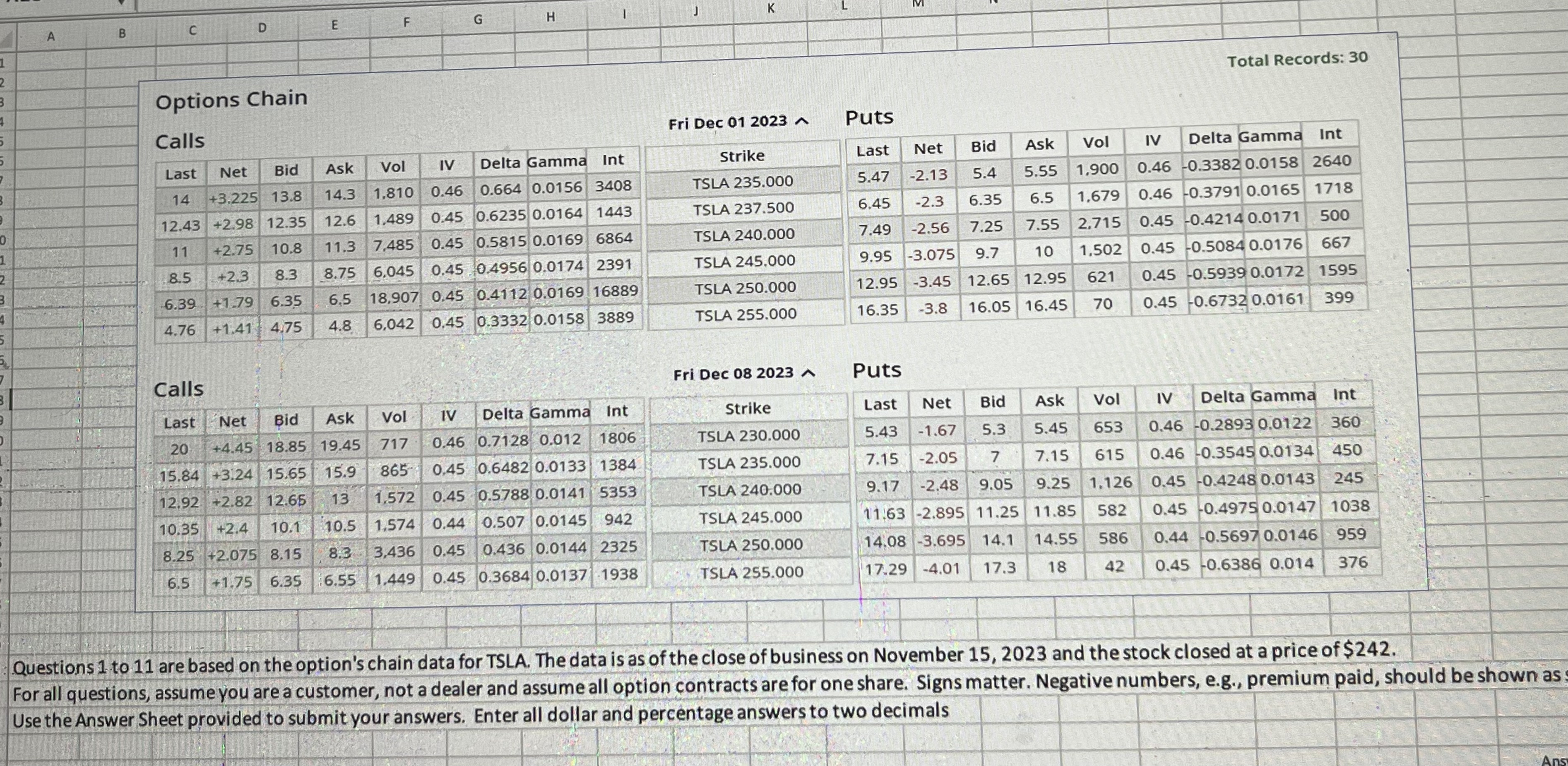

Question: 1 7 Using the information from the previous question, calculate the price of the put ( same expiry and strike ) using put - call

Using the information from the previous question, calculate the price of the put same expiry and strike using putcall parity.

Based on put call parity, write the equation for synthetic long call.

For example, a synthetic long stock would be written as: S CXertp

Based on put call parity, write the equation for synthetic long put.

For example, a synthetic long stock would be written as: S CXertp

Estimate the upfactor, used in the binomial option pricing model, for a six month option assuming annual volatility is

Assume JPM is currently trading at $ A three month call option, stuck at $ is available for $ What is the intrinsic value of this call option?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock