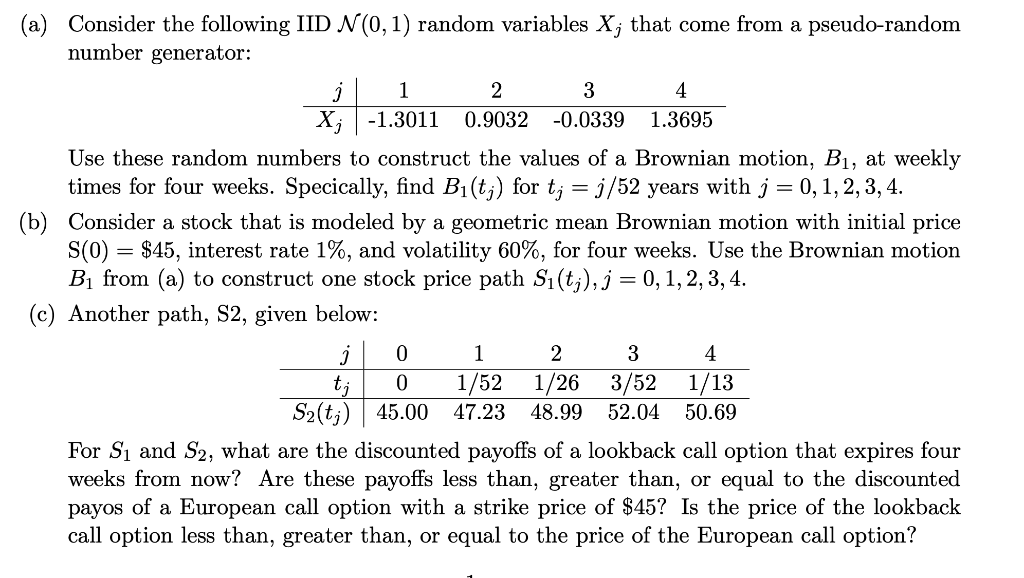

Question: 1 = (a) Consider the following IID N(0,1) random variables X; that come from a pseudo-random number generator: i 2 3 4 X; -1.3011 0.9032

1 = (a) Consider the following IID N(0,1) random variables X; that come from a pseudo-random number generator: i 2 3 4 X; -1.3011 0.9032 -0.0339 1.3695 Use these random numbers to construct the values of a Brownian motion, B1, at weekly times for four weeks. Specically, find Bi(tj) for t; = j/52 years with j = 0, 1, 2, 3, 4. (b) Consider a stock that is modeled by a geometric mean Brownian motion with initial price S(0) = $45, interest rate 1%, and volatility 60%, for four weeks. Use the Brownian motion By from (a) to construct one stock price path Si(tj), j = 0, 1, 2, 3, 4. (c) Another path, S2, given below: j 0 1 2 3 4 tj 0 1/52 1/26 3/52 1/13 S2(tj) 45.00 47.23 48.99 52.04 50.69 For Si and S2, what are the discounted payoffs of a lookback call option that expires four weeks from now? Are these payoffs less than, greater than, or equal to the discounted payos of a European call option with a strike price of $45? Is the price of the lookback call option less than, greater than, or equal to the price of the European call option? 1 = (a) Consider the following IID N(0,1) random variables X; that come from a pseudo-random number generator: i 2 3 4 X; -1.3011 0.9032 -0.0339 1.3695 Use these random numbers to construct the values of a Brownian motion, B1, at weekly times for four weeks. Specically, find Bi(tj) for t; = j/52 years with j = 0, 1, 2, 3, 4. (b) Consider a stock that is modeled by a geometric mean Brownian motion with initial price S(0) = $45, interest rate 1%, and volatility 60%, for four weeks. Use the Brownian motion By from (a) to construct one stock price path Si(tj), j = 0, 1, 2, 3, 4. (c) Another path, S2, given below: j 0 1 2 3 4 tj 0 1/52 1/26 3/52 1/13 S2(tj) 45.00 47.23 48.99 52.04 50.69 For Si and S2, what are the discounted payoffs of a lookback call option that expires four weeks from now? Are these payoffs less than, greater than, or equal to the discounted payos of a European call option with a strike price of $45? Is the price of the lookback call option less than, greater than, or equal to the price of the European call option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts