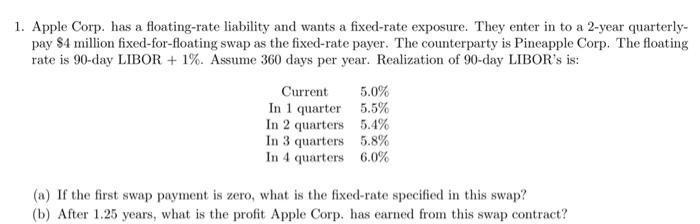

Question: 1. Apple Corp. has a floating-rate liability and wants a fixed-rate exposure. They enter in to a 2-year quarterlypay $4 million fixed-for-floating swap as the

1. Apple Corp. has a floating-rate liability and wants a fixed-rate exposure. They enter in to a 2-year quarterlypay $4 million fixed-for-floating swap as the fixed-rate payer. The counterparty is Pineapple Corp. The floating rate is 90 -day LIBOR +1%. Assume 360 days per year. Realization of 90 -day LIBOR's is: (a) If the first swap payment is zero, what is the fixed-rate specified in this swap? (b) After 1.25 years, what is the profit Apple Corp. has earned from this swap contract

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock