Question: 1. Assuming Tottenham Hotspurs continue in their current stadium following their current player strategy: Perform a DCF analysis using the cash flow projections given in

1. Assuming Tottenham Hotspurs continue in their current stadium following their current player strategy:

- Perform a DCF analysis using the cash flow projections given in the case. Based on this DCF analysis, what is the value of the Hotspurs?

- Perform a multiple analysis. Based on the multiples analysis, is the value of Tottenham any different?

- At its current stock price of13.80, is Tottenham fairly valued?

2. Using a DCF approach, evaluate each of the following decisions:

- Build the new stadium

- Sign a new striker

- Build the new stadium and sign a new striker

3. Based on the results from 2, select a best choice and provide a logical argument to support it.

Hints:

- There are multiple ways to find the answer; individual's answers may vary. Be sure to provide a logical reasoning for your assumptions.

- Exhibit 5 provides values for Discounted Cash Flows

- DCF can be done a couple ways, based on EBITDA or calculating Free Cash Flows

- If you use the Free Cash Flow Method, you will also need to include capital acquisitions by year and change the net working capital by year

- Regardless of method, you need to determine a terminal value of the business (the present value of a perpetuity)

- Use 10.25% as the discount rate

- Remember to determine the value you will need to subtract the value for debt

- For adding a new stadium and new striker, you need to adjust your original DCF model and find the new cash flows. Remember to adjust for related revenues and expenses and recalculate the value of the enterprise.

- Assume the Weighted Average Cost of Capital (WACC) is 10.25%

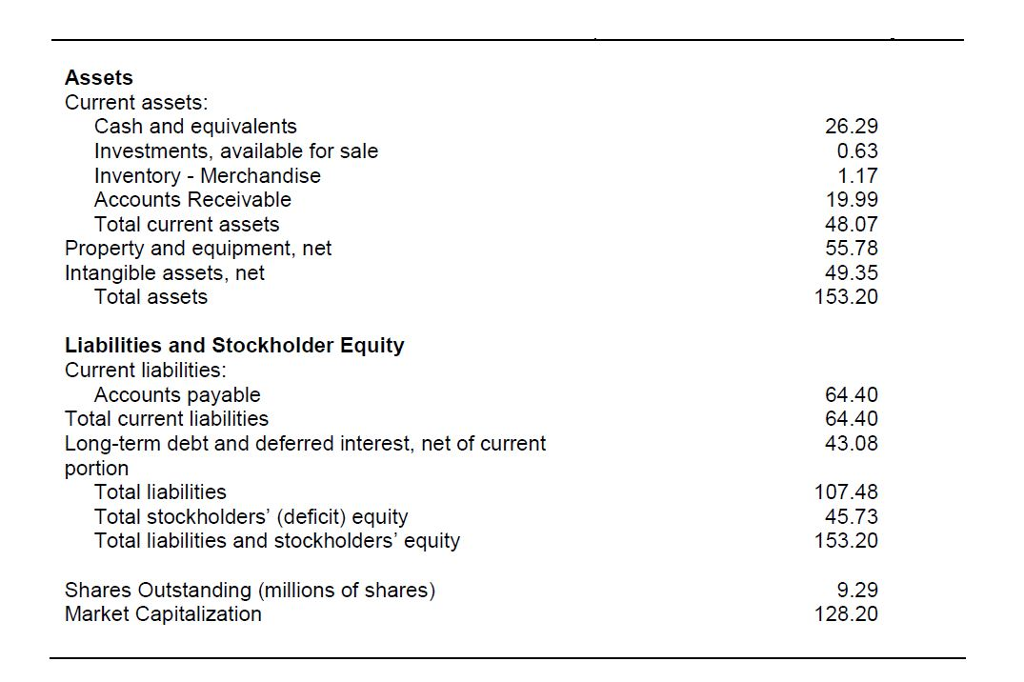

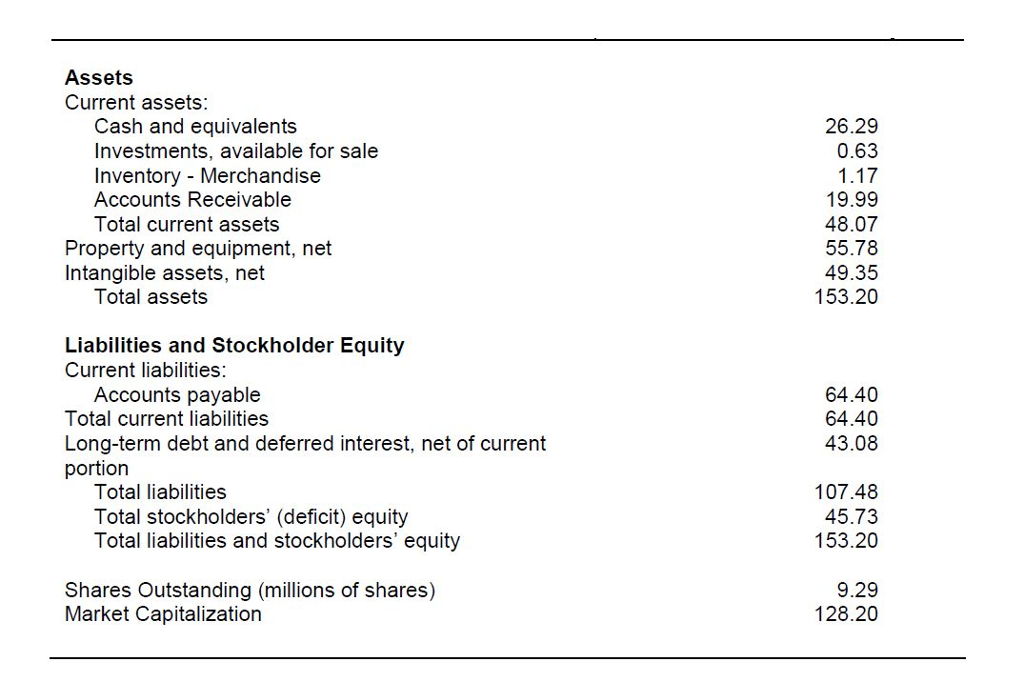

Exhibit 5

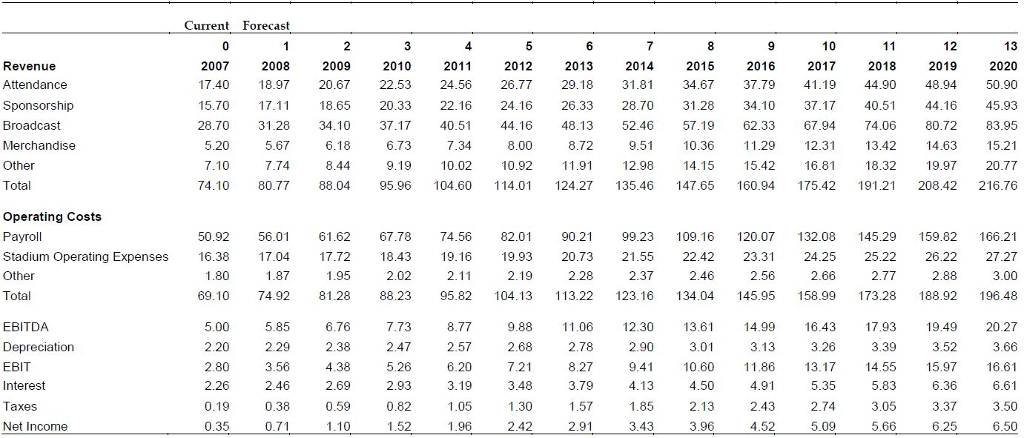

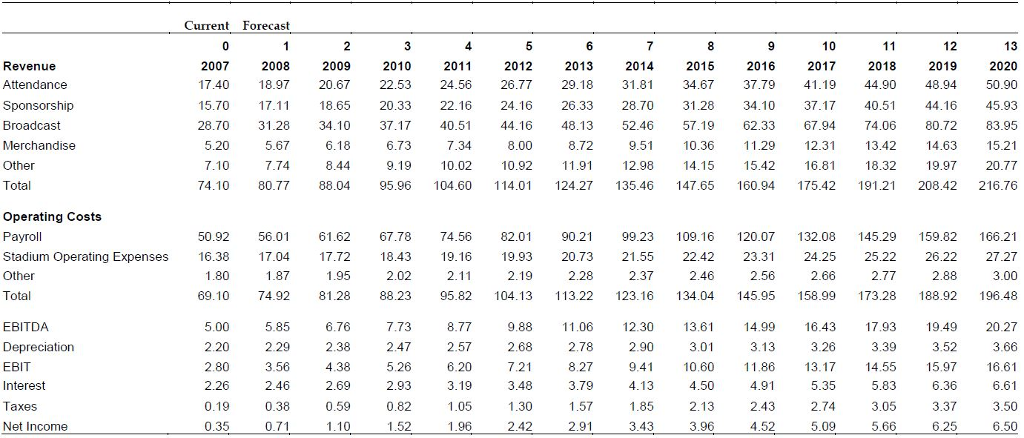

Exhibit 4

Assets Current assets: Cash and equivalents 26.29 Investments, available for sale 0.63 Inventory - Merchandise 1.17 Accounts Receivable 19.99 Total current assets 48.07 Property and equipment, net 55.78 Intangible assets. net 49.35 Total assets 153.20 Liabilities and Stockholder Equity Current liabilities: Accounts payable 64.40 Total current liabilities 64.40 Long-term debt and deferred interest, net of current 43.08 portion Total liabilities 107.48 Total stockholders' (decit) equity 45.73 Total liabilities and stockholders' equity 153.20 Shares Outstanding (millions of shares) 9.29 Market Capitalization 128.20 Ewan us- Attendance Sponsorship Broadcast Merchandise Other Total Oparatlng Coats Payroll Stadium Operating Expenses Other Total EBITDA Depreciation EBIT Interest Taxes N91 Income 2007 17.40 15.70 23.70 5.20 7.10 74.1 I] 50.92 16.33 1.80 39.1 0 5.00 2.20 2.30 2.26 0.19 0.35 Funds! 1 2003 13.97 1 7.11 31 .23 5.67 7.74 30.77 56.01 1 7.04 1.37 74.92 5.65 2.29 3.56 2.46 0.33 0.71 2 2009 20.67 13.65 34.1 I] 6.1 3 3.44 33.04 61.62 17.72 1 .95 61.23 6.76 2.33 4.33 2.69 0.59 1.10 3 2010 22.53 20.33 37.17 6.73 9.19 95.96 67.73 13.43 2.02 33.23 7.73 2.47 5.25 2.93 0.32 1.52 4 2011 24. 56 22.16 40. 51 1.34 10.02 104.60 74. 56 19.16 2.11 95.62 6.77 2.57 6.20 3.19 1.05 1.96 5 2012 26.77 24.16 44.16 3.00 10.92 114.01 32.01 19.93 2.19 104.13 9.83 2.63 7.21 3.43 1.30 2.42 6 2013 29.13 26.33 43.13 3.72 11.91 124.27 90.21 20.73 2.28 113.22 11 .06 2.73 3.27 3.79 1.57 2.91 2014 31.31 23.70 52.46 9.51 12.93 135.46 99.23 21.55 2.37 123.16 12.30 2.90 9.41 4.13 1.35 3.43 2015 34.67 31.23 57.19 10.36 14.15 147.65 109.16 22.42 2.46 134.04 13.61 3.01 10.60 4.50 2.13 3.96 2010 37.79 34.10 62.33 1 1.29 1 5.42 160.94 120.07 23.31 2.56 145.95 14.99 3.13 1 1.36 4.91 2.43 4.52 10 2017 41.19 37.17 67.94 12.31 16.31 175.42 132.03 24 .25 2.63 156.99 16.46 3.26 13.17 5.35 2.74 5.09 11 2013 44.90 40.51 74.06 13.42 13.32 1 91.21 145.29 25.22 2.77 173.28 17.93 3.39 14.55 5.63 3.05 5.66 12 2019 48.94 44.16 30.72 14.63 19.97 203.42 159.32 26.22 2.68 188.92 19.49 3.52 15.97 6.36 3.37 6.25 13 2020 50.90 45.93 33.95 15.21 20.77 216.76 166.21 27.27 3.00 196.43 20.27 3.66 16.31 6.61 3.50 6.50

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts