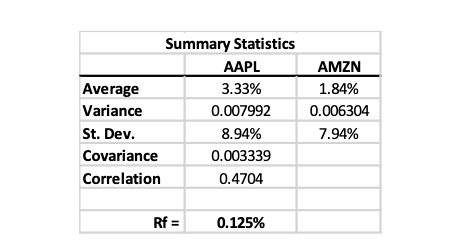

Question: 1. Based on the table above, what is the expected return of the portfolio with 0.?0 invested in AAPL and 0.3{} in AMEN? a. 1.84%.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts