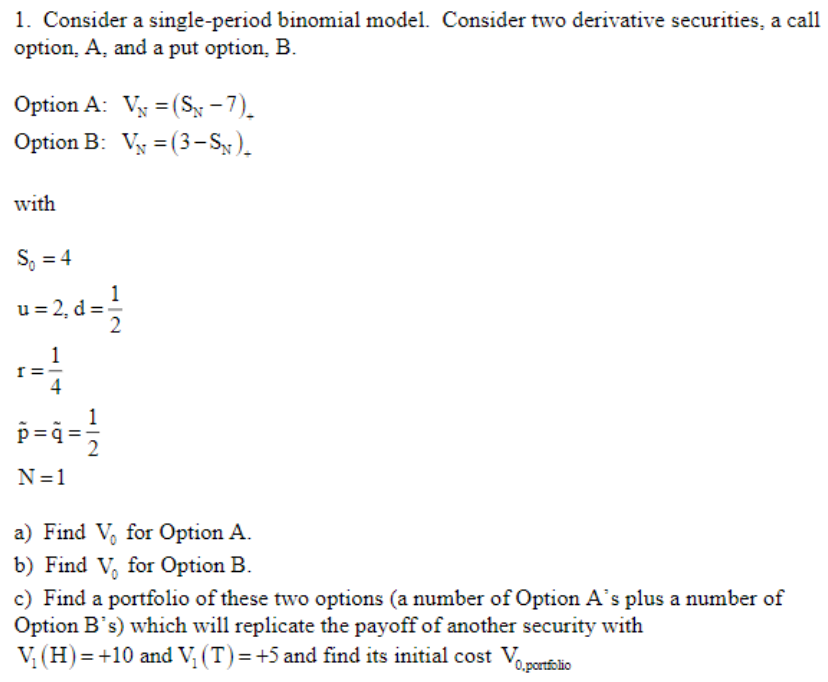

Question: 1. Consider a single-period binomial model. Consider two derivative securities, a call option, A, and a put option, B. Option A: Vx = (Sy-7). Option

1. Consider a single-period binomial model. Consider two derivative securities, a call option, A, and a put option, B. Option A: Vx = (Sy-7). Option B: Vx =(3-). with So = 4 u = 2, d = 1 =q=1 N =1 a) Find V, for Option A. b) Find V, for Option B. c) Find a portfolio of these two options (a number of Option A's plus a number of Option B's) which will replicate the payoff of another security with V (H) = +10 and V. (T) = +5 and find its initial cost V asilio 1. Consider a single-period binomial model. Consider two derivative securities, a call option, A, and a put option, B. Option A: Vx = (Sy-7). Option B: Vx =(3-). with So = 4 u = 2, d = 1 =q=1 N =1 a) Find V, for Option A. b) Find V, for Option B. c) Find a portfolio of these two options (a number of Option A's plus a number of Option B's) which will replicate the payoff of another security with V (H) = +10 and V. (T) = +5 and find its initial cost V asilio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts