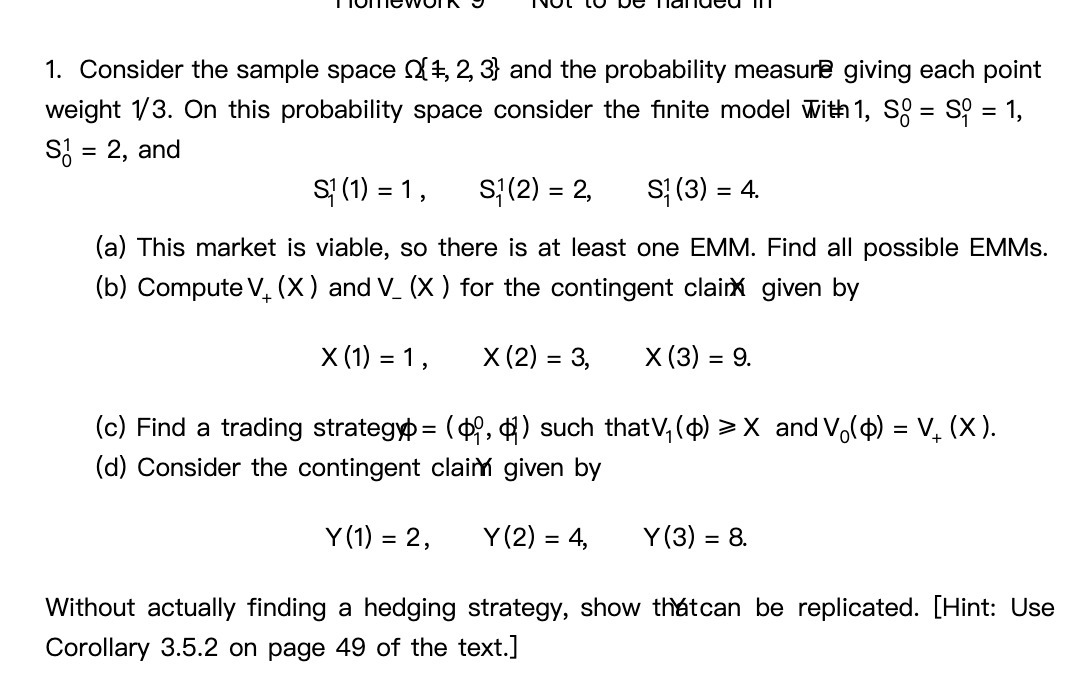

Question: 1. Consider the sample space ( 1, 2, 3) and the probability measure giving each point weight 1/3. On this probability space consider the finite

1. Consider the sample space ( 1, 2, 3) and the probability measure giving each point weight 1/3. On this probability space consider the finite model with 1, SO = $9 = 1, S! = 2, and S1 (1) = 1, S1 (2) = 2, S1 (3) = 4. (a) This market is viable, so there is at least one EMM. Find all possible EMMs. (b) Compute V. (X ) and V_ (X ) for the contingent clair given by X (1) = 1, X(2) = 3, X (3) = 9. (c) Find a trading strategy = (), ) ) such thatV, ()

1. Consider the sample space ( 1, 2, 3) and the probability measure giving each point weight 1/3. On this probability space consider the finite model with 1, SO = $9 = 1, S! = 2, and S1 (1) = 1, S1 (2) = 2, S1 (3) = 4. (a) This market is viable, so there is at least one EMM. Find all possible EMMs. (b) Compute V. (X ) and V_ (X ) for the contingent clair given by X (1) = 1, X(2) = 3, X (3) = 9. (c) Find a trading strategy = (), ) ) such thatV, ()

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts