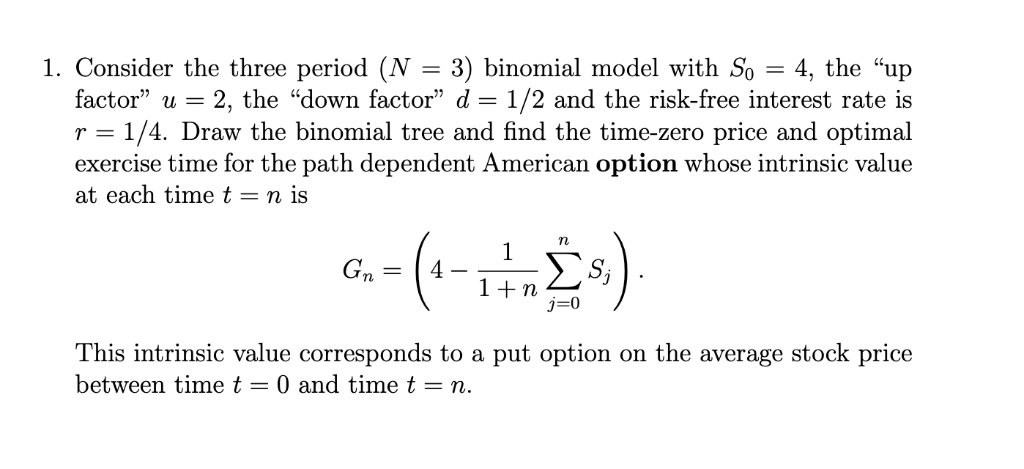

Question: 1. Consider the three period (N -3) binomial model with So-4, the up factor u-2, the down factor d- 1/2 and the risk-free interest rate

1. Consider the three period (N -3) binomial model with So-4, the "up factor" u-2, the "down factor" d- 1/2 and the risk-free interest rate is Draw the binomial tree and find the time-zero price and optimal exercise time for the path dependent American option whose intrinsic value at each time t = n is Tn Tn This intrinsic value corresponds to a put option on the average stock price between time t -0 and time t -n. 1. Consider the three period (N -3) binomial model with So-4, the "up factor" u-2, the "down factor" d- 1/2 and the risk-free interest rate is Draw the binomial tree and find the time-zero price and optimal exercise time for the path dependent American option whose intrinsic value at each time t = n is Tn Tn This intrinsic value corresponds to a put option on the average stock price between time t -0 and time t -n

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts