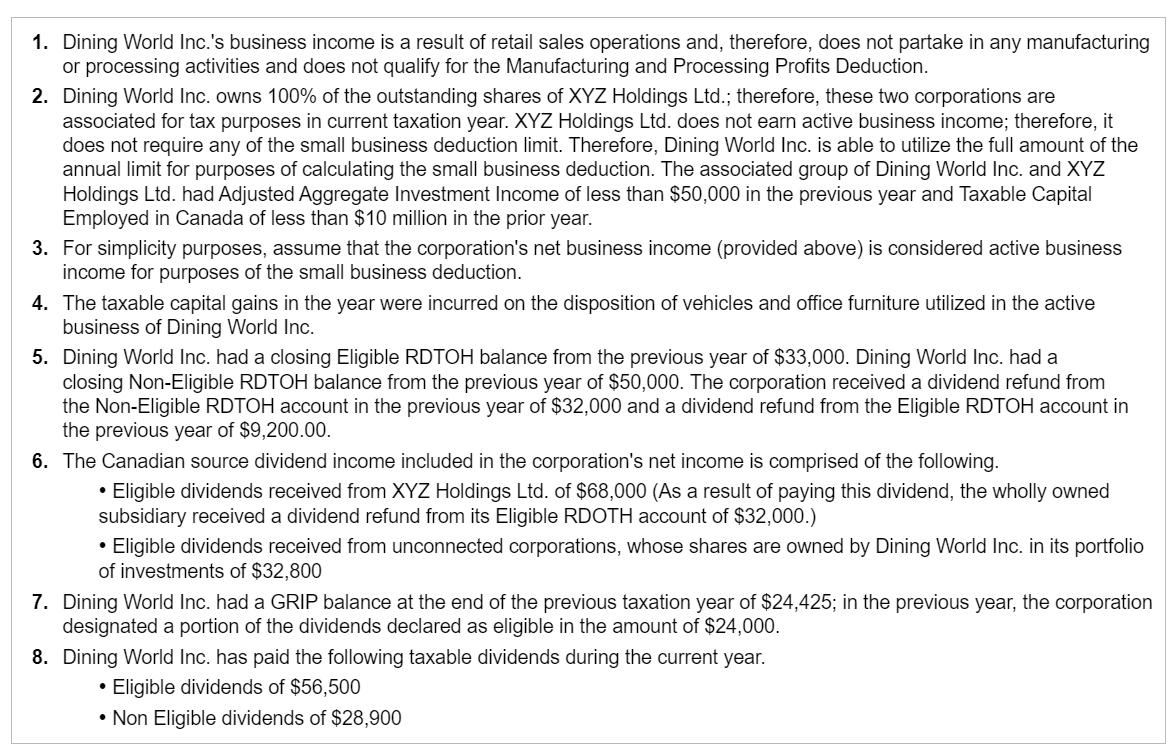

1. Dining World Inc.'s business income is a result of retail sales operations and, therefore, does...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

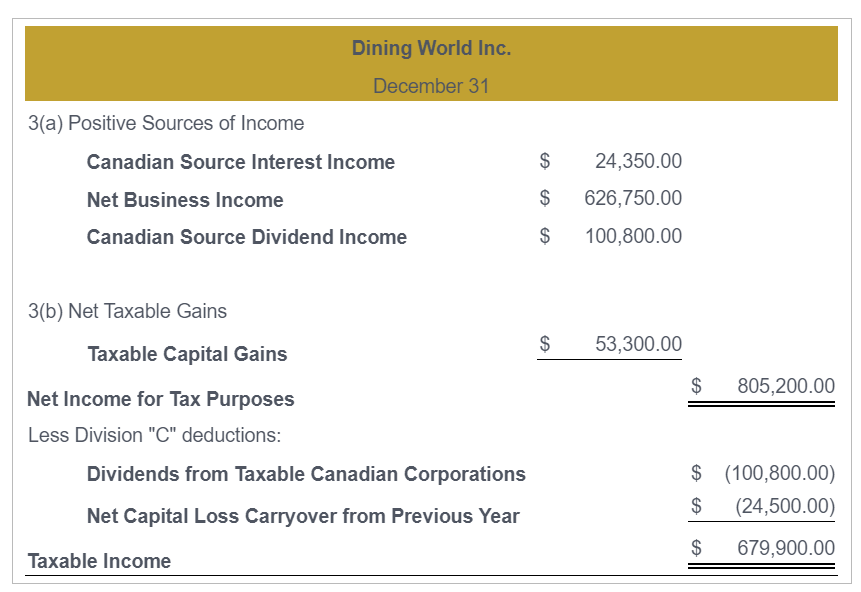

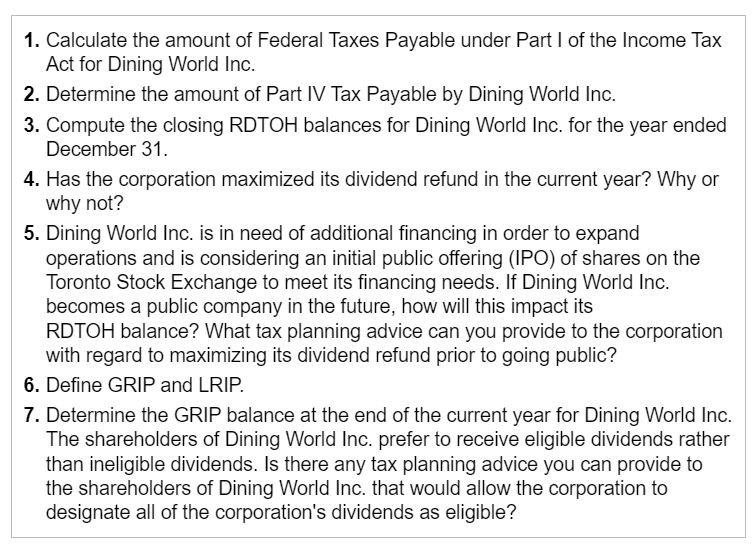

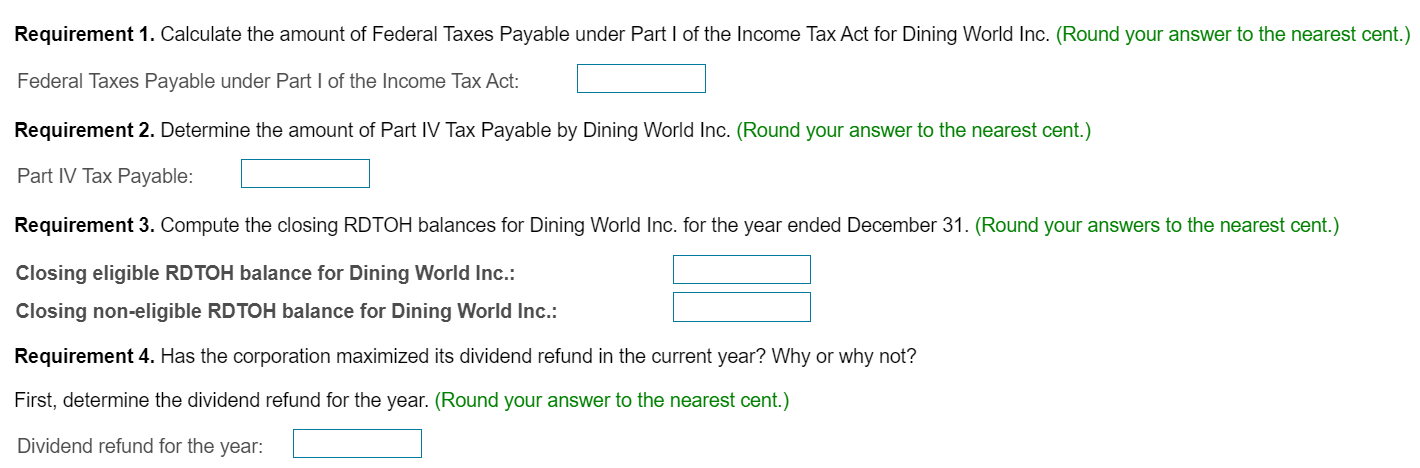

1. Dining World Inc.'s business income is a result of retail sales operations and, therefore, does not partake in any manufacturing or processing activities and does not qualify for the Manufacturing and Processing Profits Deduction. 2. Dining World Inc. owns 100% of the outstanding shares of XYZ Holdings Ltd.; therefore, these two corporations are associated for tax purposes in current taxation year. XYZ Holdings Ltd. does not earn active business income; therefore, it does not require any of the small business deduction limit. Therefore, Dining World Inc. is able to utilize the full amount of the annual limit for purposes of calculating the small business deduction. The associated group of Dining World Inc. and XYZ Holdings Ltd. had Adjusted Aggregate Investment Income of less than $50,000 in the previous year and Taxable Capital Employed in Canada of less than $10 million in the prior year. 3. For simplicity purposes, assume that the corporation's net business income (provided above) is considered active business income for purposes of the small business deduction. 4. The taxable capital gains in the year were incurred on the disposition of vehicles and office furniture utilized in the active business of Dining World Inc. 5. Dining World Inc. had a closing Eligible RDTOH balance from the previous year of $33,000. Dining World Inc. had a closing Non-Eligible RDTOH balance from the previous year of $50,000. The corporation received a dividend refund from the Non-Eligible RDTOH account in the previous year of $32,000 and a dividend refund from the Eligible RDTOH account in the previous year of $9,200.00. 6. The Canadian source dividend income included in the corporation's net income is comprised of the following. • Eligible dividends received from XYZ Holdings Ltd. of $68,000 (As a result of paying this dividend, the wholly owned subsidiary received a dividend refund from its Eligible RDOTH account of $32,000.) • Eligible dividends received from unconnected corporations, whose shares are owned by Dining World Inc. in its portfolio of investments of $32,800 7. Dining World Inc. had a GRIP balance at the end of the previous taxation year of $24,425; in the previous year, the corporation designated a portion of the dividends declared as eligible in the amount of $24,000. 8. Dining World Inc. has paid the following taxable dividends during the current year. . Eligible dividends of $56,500 • Non Eligible dividends of $28,900 Dining World Inc. December 31 3(a) Positive Sources of Income Canadian Source Interest Income Net Business Income $ 24,350.00 $ 626,750.00 Canadian Source Dividend Income $ 100,800.00 3(b) Net Taxable Gains Taxable Capital Gains Net Income for Tax Purposes $ 53,300.00 $ 805,200.00 Less Division "C" deductions: Dividends from Taxable Canadian Corporations $ (100,800.00) $ (24,500.00) Net Capital Loss Carryover from Previous Year Taxable Income $ 679,900.00 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc. 2. Determine the amount of Part IV Tax Payable by Dining World Inc. 3. Compute the closing RDTOH balances for Dining World Inc. for the year ended December 31. 4. Has the corporation maximized its dividend refund in the current year? Why or why not? 5. Dining World Inc. is in need of additional financing in order to expand operations and is considering an initial public offering (IPO) of shares on the Toronto Stock Exchange to meet its financing needs. If Dining World Inc. becomes a public company in the future, how will this impact its RDTOH balance? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? 6. Define GRIP and LRIP. 7. Determine the GRIP balance at the end of the current year for Dining World Inc. The shareholders of Dining World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Dining World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? Dining World Inc. is a Canadian controlled private corporation (CCPC) that operates a retail business selling cooking utensils, knives, and small appliances for both professional chefs and home cooks. Dining World Inc. is operated out of Ottawa, Ontario, and all of the corporation's revenue and expenses are incurred in Ontario. Requirement 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc. (Round your answer to the nearest cent.) Federal Taxes Payable under Part I of the Income Tax Act: Requirement 2. Determine the amount of Part IV Tax Payable by Dining World Inc. (Round your answer to the nearest cent.) Part IV Tax Payable: Requirement 3. Compute the closing RDTOH balances for Dining World Inc. for the year ended December 31. (Round your answers to the nearest cent.) Closing eligible RDTOH balance for Dining World Inc.: Closing non-eligible RDTOH balance for Dining World Inc.: Requirement 4. Has the corporation maximized its dividend refund in the current year? Why or why not? First, determine the dividend refund for the year. (Round your answer to the nearest cent.) Dividend refund for the year: Requirement 7. Determine the GRIP balance at the end of the current year for Dining World Inc. The shareholders of Dining World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Dining World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? GRIP balance at the end of the current year: 1. Dining World Inc.'s business income is a result of retail sales operations and, therefore, does not partake in any manufacturing or processing activities and does not qualify for the Manufacturing and Processing Profits Deduction. 2. Dining World Inc. owns 100% of the outstanding shares of XYZ Holdings Ltd.; therefore, these two corporations are associated for tax purposes in current taxation year. XYZ Holdings Ltd. does not earn active business income; therefore, it does not require any of the small business deduction limit. Therefore, Dining World Inc. is able to utilize the full amount of the annual limit for purposes of calculating the small business deduction. The associated group of Dining World Inc. and XYZ Holdings Ltd. had Adjusted Aggregate Investment Income of less than $50,000 in the previous year and Taxable Capital Employed in Canada of less than $10 million in the prior year. 3. For simplicity purposes, assume that the corporation's net business income (provided above) is considered active business income for purposes of the small business deduction. 4. The taxable capital gains in the year were incurred on the disposition of vehicles and office furniture utilized in the active business of Dining World Inc. 5. Dining World Inc. had a closing Eligible RDTOH balance from the previous year of $33,000. Dining World Inc. had a closing Non-Eligible RDTOH balance from the previous year of $50,000. The corporation received a dividend refund from the Non-Eligible RDTOH account in the previous year of $32,000 and a dividend refund from the Eligible RDTOH account in the previous year of $9,200.00. 6. The Canadian source dividend income included in the corporation's net income is comprised of the following. • Eligible dividends received from XYZ Holdings Ltd. of $68,000 (As a result of paying this dividend, the wholly owned subsidiary received a dividend refund from its Eligible RDOTH account of $32,000.) • Eligible dividends received from unconnected corporations, whose shares are owned by Dining World Inc. in its portfolio of investments of $32,800 7. Dining World Inc. had a GRIP balance at the end of the previous taxation year of $24,425; in the previous year, the corporation designated a portion of the dividends declared as eligible in the amount of $24,000. 8. Dining World Inc. has paid the following taxable dividends during the current year. . Eligible dividends of $56,500 • Non Eligible dividends of $28,900 Dining World Inc. December 31 3(a) Positive Sources of Income Canadian Source Interest Income Net Business Income $ 24,350.00 $ 626,750.00 Canadian Source Dividend Income $ 100,800.00 3(b) Net Taxable Gains Taxable Capital Gains Net Income for Tax Purposes $ 53,300.00 $ 805,200.00 Less Division "C" deductions: Dividends from Taxable Canadian Corporations $ (100,800.00) $ (24,500.00) Net Capital Loss Carryover from Previous Year Taxable Income $ 679,900.00 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc. 2. Determine the amount of Part IV Tax Payable by Dining World Inc. 3. Compute the closing RDTOH balances for Dining World Inc. for the year ended December 31. 4. Has the corporation maximized its dividend refund in the current year? Why or why not? 5. Dining World Inc. is in need of additional financing in order to expand operations and is considering an initial public offering (IPO) of shares on the Toronto Stock Exchange to meet its financing needs. If Dining World Inc. becomes a public company in the future, how will this impact its RDTOH balance? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? 6. Define GRIP and LRIP. 7. Determine the GRIP balance at the end of the current year for Dining World Inc. The shareholders of Dining World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Dining World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? Dining World Inc. is a Canadian controlled private corporation (CCPC) that operates a retail business selling cooking utensils, knives, and small appliances for both professional chefs and home cooks. Dining World Inc. is operated out of Ottawa, Ontario, and all of the corporation's revenue and expenses are incurred in Ontario. Requirement 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc. (Round your answer to the nearest cent.) Federal Taxes Payable under Part I of the Income Tax Act: Requirement 2. Determine the amount of Part IV Tax Payable by Dining World Inc. (Round your answer to the nearest cent.) Part IV Tax Payable: Requirement 3. Compute the closing RDTOH balances for Dining World Inc. for the year ended December 31. (Round your answers to the nearest cent.) Closing eligible RDTOH balance for Dining World Inc.: Closing non-eligible RDTOH balance for Dining World Inc.: Requirement 4. Has the corporation maximized its dividend refund in the current year? Why or why not? First, determine the dividend refund for the year. (Round your answer to the nearest cent.) Dividend refund for the year: Requirement 7. Determine the GRIP balance at the end of the current year for Dining World Inc. The shareholders of Dining World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Dining World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? GRIP balance at the end of the current year:

Expert Answer:

Answer rating: 100% (QA)

1 Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc Round your answer to the nearest cent Part I tax calculation First 500000 of active business inc... View the full answer

Related Book For

International Marketing And Export Management

ISBN: 9781292016924

8th Edition

Authors: Gerald Albaum , Alexander Josiassen , Edwin Duerr

Posted Date:

Students also viewed these accounting questions

-

Kitchen World Inc. is a Canadian controlled private corporation (CCPC) that operates a retail business selling cooking utensils, knives and small appliances for both professional chefs and home...

-

Required a. Use professional judgment in deciding on the preliminary judgment about materiality for earnings, current assets, current liabilities, and total assets. Your conclusions should be stated...

-

An average of three small businesses go bankrupt each month. What is the probability that five small businesses will go bankrupt in a certain month?

-

Jefferson County operates a centralized motor pool to service county vehicles. At the end of 2016, the Motor Pool Internal Service Fund had the following account balances: The following events took...

-

A graph of a function is shown below. Find f(2), f(-4), and f(0). 4:2

-

Does Fairmont have any contactor personnel whose have terminated but are being paid through payroll after termination (e.g., ghost employees)?

-

On August 31, 2012, Daisy Floral Supply had a $155,000 debit balance in Accounts receivable and a $6,200 credit balance in Allowance for uncollectible accounts. During September, Daisy made Sales on...

-

To mix plaster for a dental model, 45 milliliters (mL) of water are used for 100 grams (g) of plaster. How many mL of water should be used for 200 g of plaster? . A cardiopulmonary resuscitation...

-

What is the consumer-adoption process? What are the steps in the process? Discuss the consumer-adoption process in the context of the product you provided in your group assignment. NOTE: i have...

-

CASE STUDY: Jol Transport has been around since 1965, a household name with hundreds of satisfied customers. Jol Transport is based in Centurion, Gauteng, and service domestic relocations in the...

-

discuss and comment the following post : Who hasn't dreamt of winning the jackpot at least once in their life? The exhilarating idea of holding that winning ticket with numbers like 11, 7, 5, and 19...

-

How do globalization and neoliberal economic policies influence the dynamics of social class, particularly in terms of the creation of transnational elite classes and the globalization of poverty?

-

John is participating in a marathon that is 26.2 miles and he finishes in 4.5 hours. His distance, d, depends on his time, t. What is an appropriate domain for this situation?

-

Why do you think that clinical psychology is the most popular subspecialty of psychology?

-

The Xtra Store has a Human Resources Department and a Janitorial Department that provide service to three sales departments. The Human Resources Department cost is allocated on the basis of...

-

What are conversion costs? What are prime costs?

-

Government regulations can affect the viability and effectiveness of a company using the Internet as a foreign market entry mode. Contrast the government regulations governing e-commerce in the...

-

Primex Marketing, Inc., formed in 1982, is an international niche marketer of Roleez wheels and a limited line of products using the wheels. The patented wheels use very low pressure, soft, wide, and...

-

In the decade of the 2010s, the plans and operations of Avon Inc. in marketing, research, and manufacturing throughout Asia are still being affected by actions taken after a 1998 meeting. The US...

-

In a talk at the White House in December 2009, President Barack Obama argued, Ultimately in this country we rise and fall together: banks and small businesses, consumers and large corporations. Why...

-

An article in the New York Times in mid-2012 noted, with the economy still struggling and new regulations meant to eliminate bad lending, bank loans continue to lag. a. What does the article mean by...

-

What is money? Why do we need money?

Study smarter with the SolutionInn App