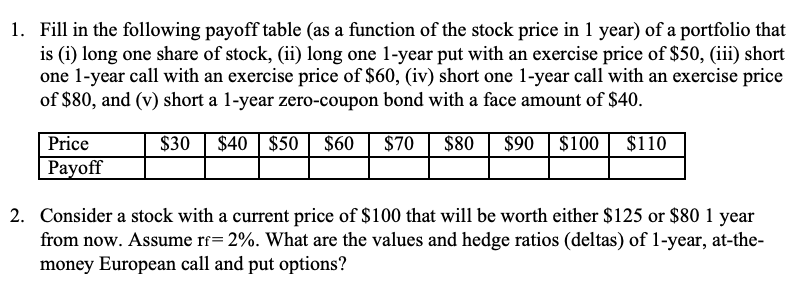

Question: 1. Fill in the following payoff table (as a function of the stock price in 1 year) of a portfolio that is (i) long

1. Fill in the following payoff table (as a function of the stock price in 1 year) of a portfolio that is (i) long one share of stock, (ii) long one 1-year put with an exercise price of $50, (iii) short one 1-year call with an exercise price of $60, (iv) short one 1-year call with an exercise price of $80, and (v) short a 1-year zero-coupon bond with a face amount of $40. Price Payoff $30 $40 $50 $60 $70 $80 $90 $100 $110 2. Consider a stock with a current price of $100 that will be worth either $125 or $80 1 year from now. Assume rf=2%. What are the values and hedge ratios (deltas) of 1-year, at-the- money European call and put options?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts