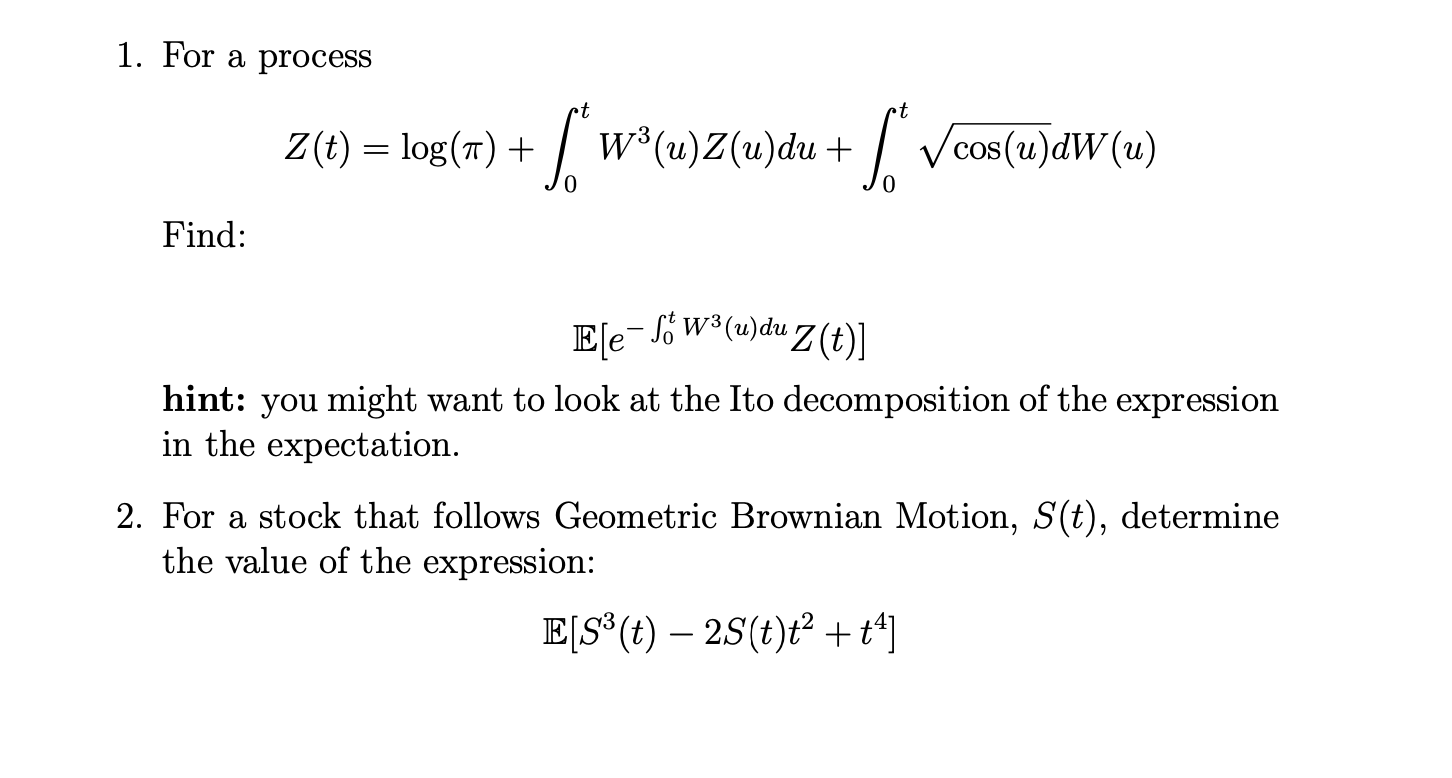

Question: 1. For a process = log ( 7 ) + [ wa (u ) Z ( u ) du + / Vcos ( u )aw

1. For a process = log ( 7 ) + [ wa (u ) Z ( u ) du + / Vcos ( u )aw ( u ) Find: Ele So w3(u)du z ( t) ] hint: you might want to look at the Ito decomposition of the expression in the expectation. 2. For a stock that follows Geometric Brownian Motion, S(t), determine the value of the expression: ELS' (t) - 2S(t) t2 + + 4 ]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock