Question: 1. Given the following binomial-tree interest rate process with given one year forward rates, determine: 1) the value of a two-year 5% coupon (annual-pay) bond;

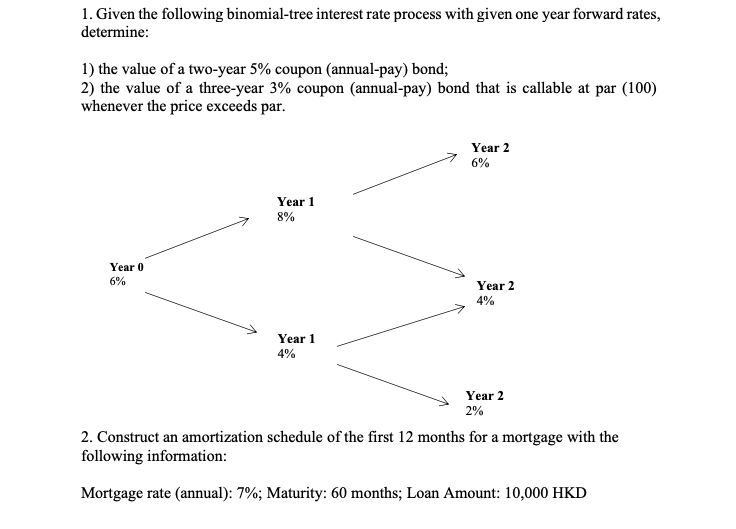

1. Given the following binomial-tree interest rate process with given one year forward rates, determine: 1) the value of a two-year 5% coupon (annual-pay) bond; 2) the value of a three-year 3% coupon (annual-pay) bond that is callable at par (100) whenever the price exceeds par. Year 2 6% Year 1 8% Year 0 6% Year 2 4% Year 1 4% Year 2 2% 2. Construct an amortization schedule of the first 12 months for a mortgage with the following information: Mortgage rate (annual): 7%; Maturity: 60 months; Loan Amount: 10,000 HKD 1. Given the following binomial-tree interest rate process with given one year forward rates, determine: 1) the value of a two-year 5% coupon (annual-pay) bond; 2) the value of a three-year 3% coupon (annual-pay) bond that is callable at par (100) whenever the price exceeds par. Year 2 6% Year 1 8% Year 0 6% Year 2 4% Year 1 4% Year 2 2% 2. Construct an amortization schedule of the first 12 months for a mortgage with the following information: Mortgage rate (annual): 7%; Maturity: 60 months; Loan Amount: 10,000 HKD

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts