Required: 1. How did the spill-related costs recognized by BP in its financial statements through 2014 differ

Question:

Required:

1. How did the spill-related costs recognized by BP in its financial statements through 2014 differ from a statistical estimate of the total expected costs that the company's senior management might have prepared and used internally over the same time frame?

a) For each category of contingent liability - environmental, litigation and claims, and Clean Water Act penalties - BP asserts that is not possible to reliability estimate the full extent of the company's ultimate economic exposure. Identify a specific reason for this uncertainty for each category.

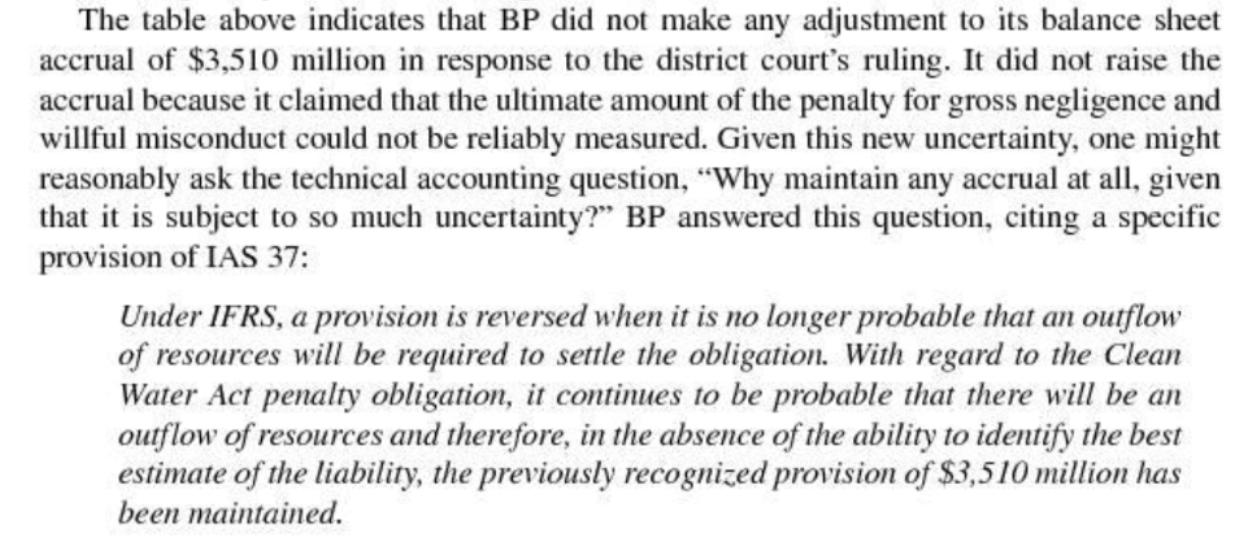

b) Why did BP maintain the $3,150 million provision for the penalty it will have to pay under the U.S. Clean Water Act after the district court's finding of gross negligence and willful misconduct called this amount into question?

c) In 2015 and 2016, BP recognized additional spill-related costs of $18.6 billion, bringing the total cumulative costs recognized across the four categories to over $66 billion. Based on the above information, make an informed guess about how these newly recognized costs were distributed across the four cost categories. How might accounting recognition and disclosure of contingent liabilities be improved to enable readers to formulate better estimates?

Expert Answer:

1 Although statistical estimates factor into the recognition of contingent liabilities accounting rules preclude recognition of contingent liabilities that are either less than probable or cannot be r... View the full answer

Financial Accounting

ISBN: 978-0133427530

10th edition

Authors: Walter Harrison, Charles Horngren, William Thomas