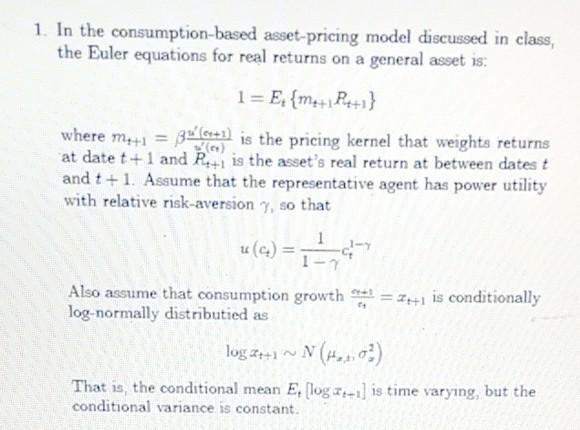

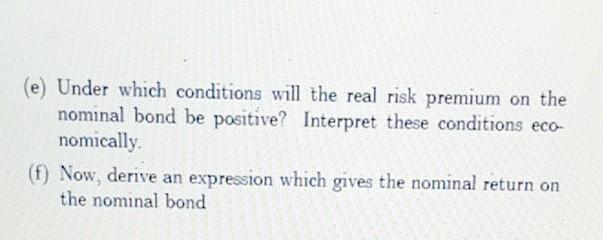

Question: 1. In the consumption-based asset-pricing model discussed in class, the Euler equations for real returns on a general asset is: 1 = E:{met Petr where

1. In the consumption-based asset-pricing model discussed in class, the Euler equations for real returns on a general asset is: 1 = E:{met Petr where mu+1 = 35 (6+1) is the pricing kernel that weights returns at date t +1 and Pet is the asset's real return at between datest and t + 1. Assume that the representative agent has power utility with relative risk-aversion, so that 1 Also assume that consumption growth = 2+1 is conditionally log-normally distributied as log t+1 ~ N(H2_, 03) That is the conditional mean Elog Tu-1) is time varying, but the conditional variance is constant. (e) Under which conditions will the real risk premium on the nominal bond be positive? Interpret these conditions eco- nomically (1) Now, derive an expression which gives the nominal return on the nominal bond 1. In the consumption-based asset-pricing model discussed in class, the Euler equations for real returns on a general asset is: 1 = E:{met Petr where mu+1 = 35 (6+1) is the pricing kernel that weights returns at date t +1 and Pet is the asset's real return at between datest and t + 1. Assume that the representative agent has power utility with relative risk-aversion, so that 1 Also assume that consumption growth = 2+1 is conditionally log-normally distributied as log t+1 ~ N(H2_, 03) That is the conditional mean Elog Tu-1) is time varying, but the conditional variance is constant. (e) Under which conditions will the real risk premium on the nominal bond be positive? Interpret these conditions eco- nomically (1) Now, derive an expression which gives the nominal return on the nominal bond

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts