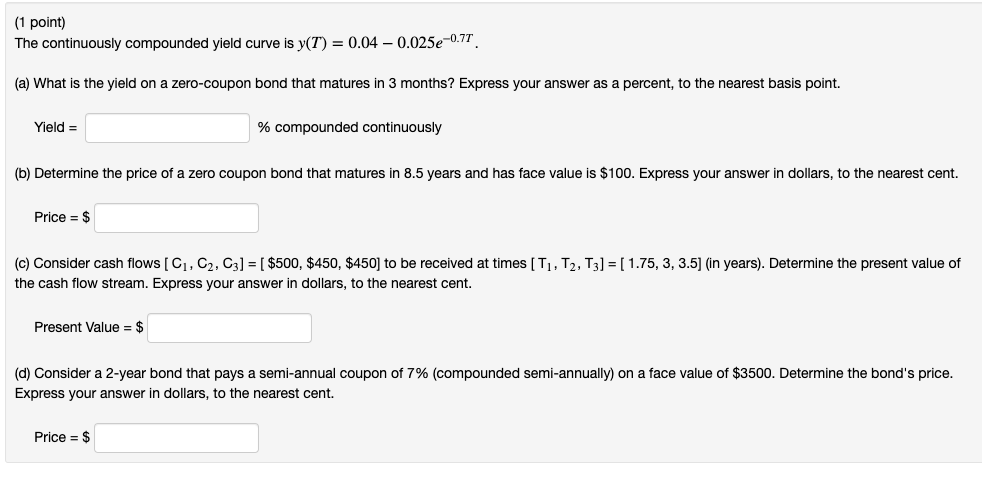

Question: (1 point) The continuously compounded yield curve is y(T) = 0.04 -0.025e-0.77 (a) What is the yield on a zero-coupon bond that matures in 3

(1 point) The continuously compounded yield curve is y(T) = 0.04 -0.025e-0.77 (a) What is the yield on a zero-coupon bond that matures in 3 months? Express your answer as a percent, to the nearest basis point. Yield = % compounded continuously (b) Determine the price of a zero coupon bond that matures in 8.5 years and has face value is $100. Express your answer in dollars, to the nearest cent. Price = $ (c) Consider cash flows (C1, C2, C3] = [ $500, $450, $450] to be received at times [T1, T2, T3] = [ 1.75, 3, 3.5] (in years). Determine the present value of the cash flow stream. Express your answer in dollars, to the nearest cent. Present Value = $ (d) Consider a 2-year bond that pays a semi-annual coupon of 7% (compounded semi-annually) on a face value of $3500. Determine the bond's price. Express your answer in dollars, to the nearest cent. Price = $

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts