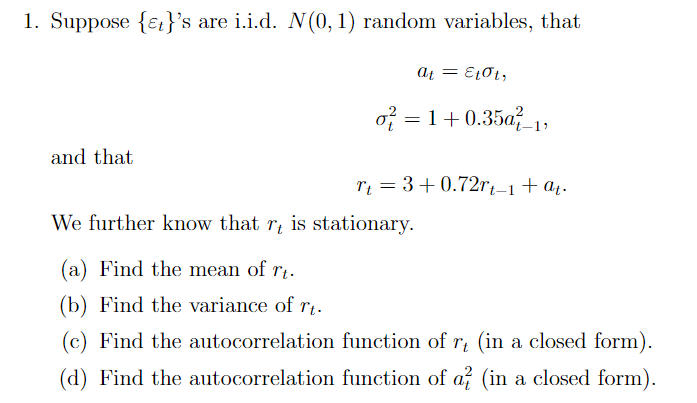

Question: 1. Suppose {et}'s are i.i.d. N(0, 1) random variables, that at = EtOt, ? = 1 +0.3501-1, and that r = 3+ 0.72re-1+ at. We

1. Suppose {et}'s are i.i.d. N(0, 1) random variables, that at = EtOt, "? = 1 +0.3501-1, and that r = 3+ 0.72re-1+ at. We further know that r, is stationary. (a) Find the mean of rt. (b) Find the variance of rt. (c) Find the autocorrelation function of r (in a closed form). (d) Find the autocorrelation function of a, (in a closed form)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock