Question: can you please solve this question please? its time series on arch and garch process ithink 3. Suppose rt is such that H = 180

can you please solve this question please? its time series on arch and garch process ithink

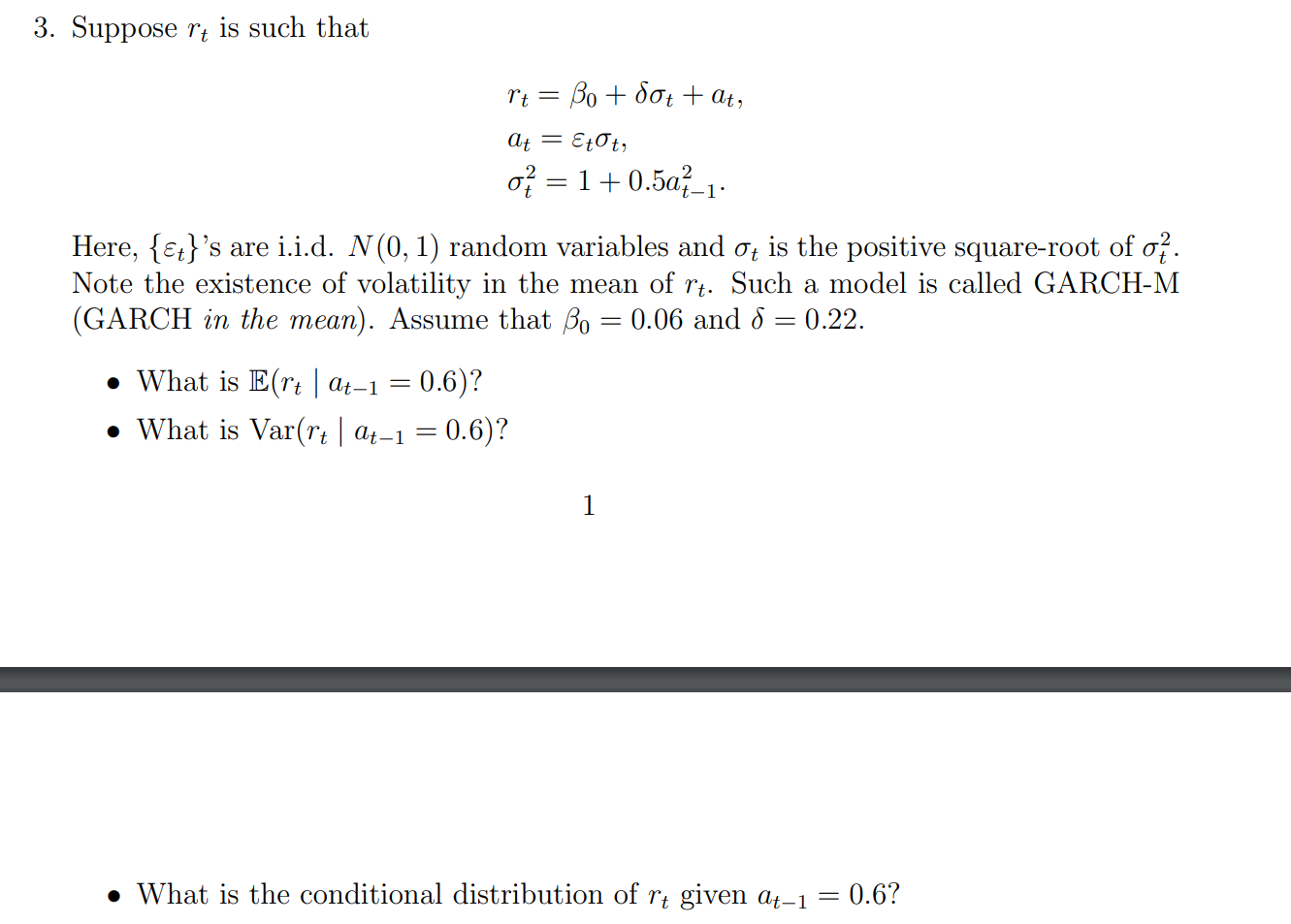

3. Suppose rt is such that H = 180 + 50': + at: at = 5:501: 2 _ 2 (It 1+ 0.5at_1. Here, {5t}'s are i.i.d. N (0, 1) random variables and at is the positive squareroot of of. Note the existence of volatility in the mean of rt. Such a model is called GARCHM [GARCH m the mean). Assume that ,80 = 0.06 and 6 = 0.22. o What is EU} | at_1 = 0.6)? o What is Varm | at_1 = 0.6)? o What is the conditional distribution of rt given at_1 = 0.6

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock