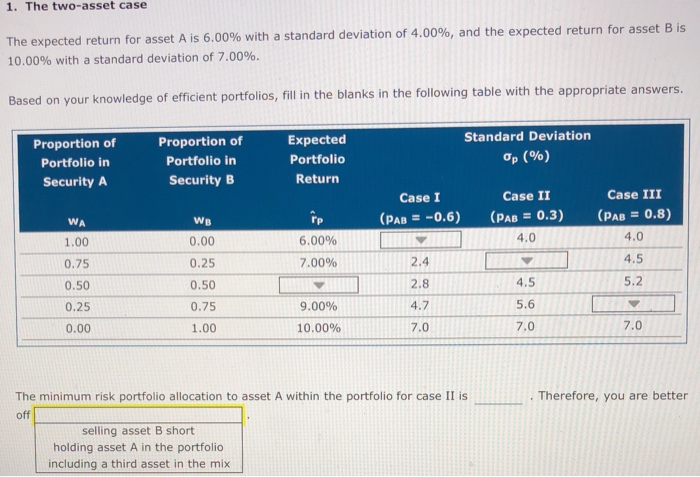

Question: 1. The two-asset Case The expected return for asset A is 6.00% with a standard deviation of 4.00%, and the expected return for asset B

1. The two-asset Case The expected return for asset A is 6.00% with a standard deviation of 4.00%, and the expected return for asset B is 10.00% with a standard deviation of 7.00%. Based on your knowledge of efficient portfolios, fill in the blanks in the following table with the appropriate answers. Proportion of Portfolio in Security A Proportion of Portfolio in Security B Expected Portfolio Return Standard Deviation Op (%) Case I (PAB = -0.6) WB Case II (PAB = 0.3) 4.0 WA 1.00 0.75 0.50 0.25 0.00 0.00 0.25 0.50 6.00% 7.00% Case III (PAB = 0.8) 4.0 4.5 5.2 2.4 2.8 4.5 5.6 0.75 4. 9.00% 10.00% 1.00 7.0 Therefore, you are better The minimum risk portfolio allocation to asset A within the portfolio for case II is off selling asset B short holding asset A in the portfolio including a third asset in the mix

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts