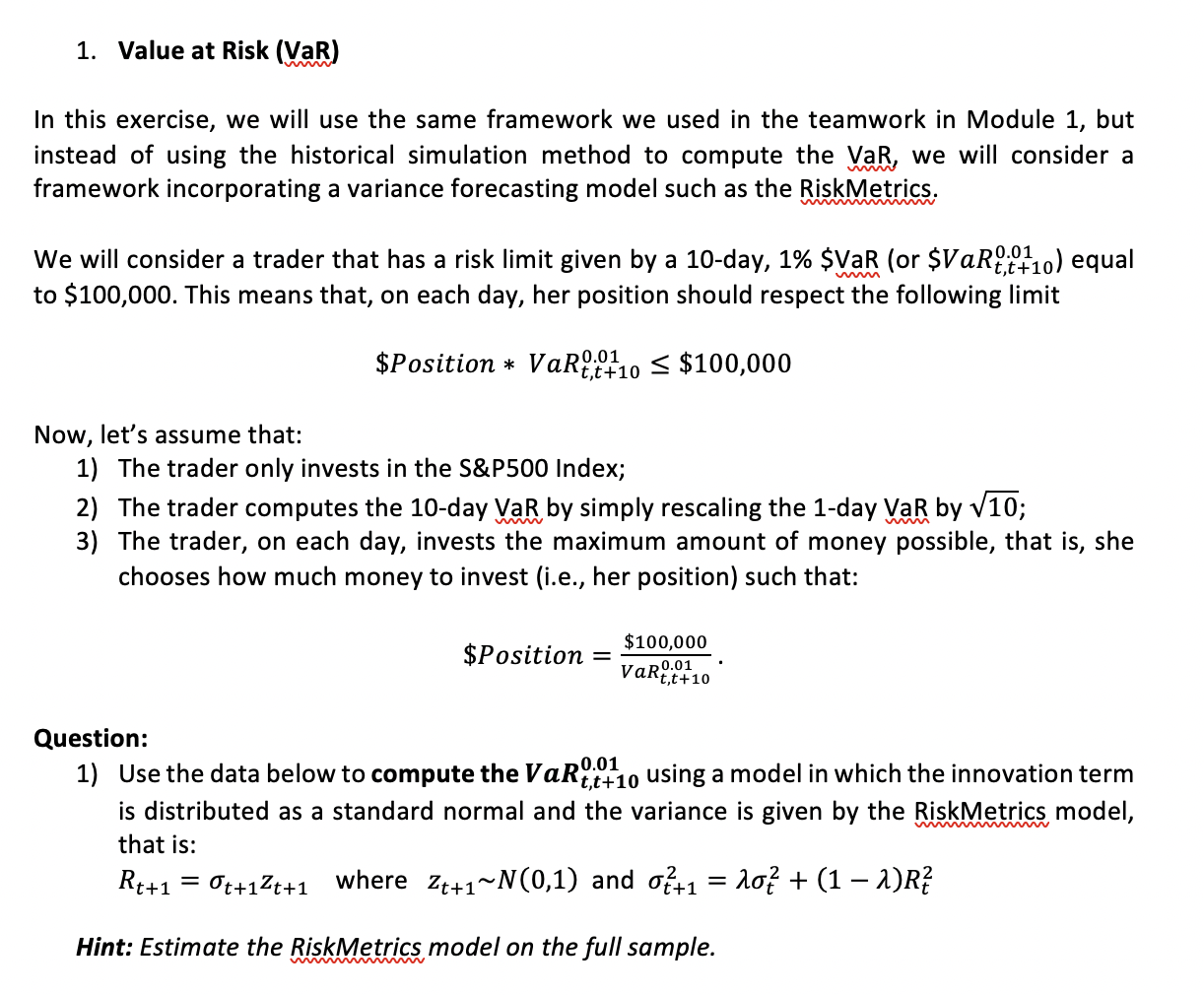

Question: 1. Value at Risk (VaR) In this exercise, we will use the same framework we used in the teamwork in Module 1, but instead of

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts