Question: 1. What are the control variables? 2. What are the state variables? 3. Write the Lagrangian function for this problem. 4. Write the Bellman equation

1. What are the control variables?

2. What are the state variables?

3. Write the Lagrangian function for this problem.

4. Write the Bellman equation for this problem.

5. Find the first-order condition(s)

6. Find the envelope condition(s)

7. Find the Euler equation

8. Provide a guess for the value function.

9. Derive the policy functions using your guess.

10. Interpret your results.

11. Solve for the steady-state of: (a). capital (b). consumption.

12. Assuming =0.5 and =0.9, calculate the steady-state value of: (a) capital (b) consumption

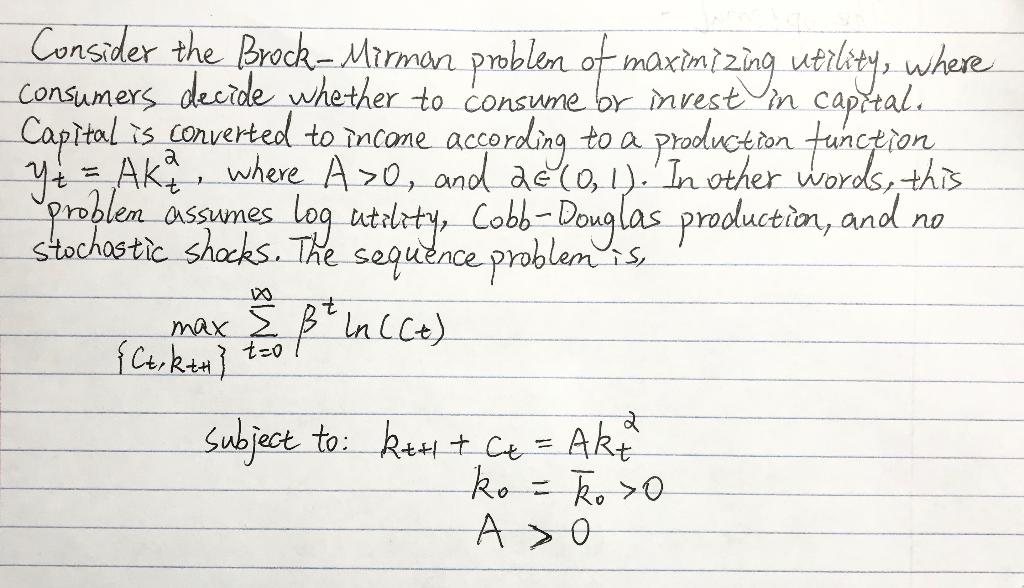

ction Consider the Brock-Mirman problem of maximizing utility, where consumers decide whether to consume br invest in capitale Capital is converted to incone according to a yt = Ake, where A>0, and a (0,1). In other words, this stochastic shocks. The sequence problem is, problem assumes log utelity, Cobb- Douglas production, and no max I Bln (Ct) { Cirkth} subject to ket+ Ce = Akt ko - hexo A>O * t=0 ction Consider the Brock-Mirman problem of maximizing utility, where consumers decide whether to consume br invest in capitale Capital is converted to incone according to a yt = Ake, where A>0, and a (0,1). In other words, this stochastic shocks. The sequence problem is, problem assumes log utelity, Cobb- Douglas production, and no max I Bln (Ct) { Cirkth} subject to ket+ Ce = Akt ko - hexo A>O * t=0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts