Question: 1. You are attempting to construct a minimum variance portfolio (MVP) with two well-diversified funds, S and B. The following table contains relevant information:

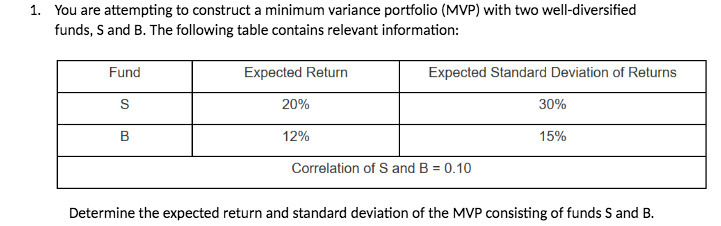

1. You are attempting to construct a minimum variance portfolio (MVP) with two well-diversified funds, S and B. The following table contains relevant information: Fund S B Expected Return 20% 12% Expected Standard Deviation of Returns 30% 15% Correlation of S and B = 0.10 Determine the expected return and standard deviation of the MVP consisting of funds S and B.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock