Question: 1) Your asset allocation benchmark has 5 asset classes: US large stocks, US small stocks, EAFE Equity, EM Equity, and REITS. The corresponding benchmark

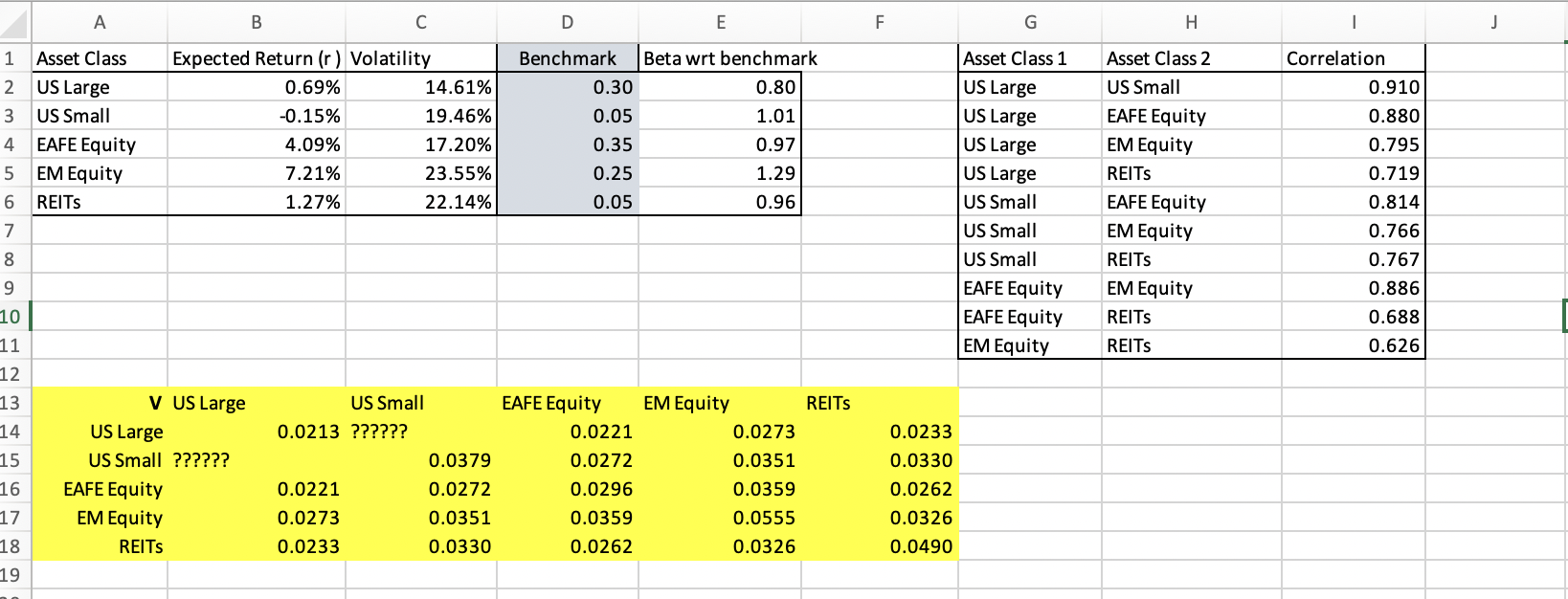

1) Your asset allocation benchmark has 5 asset classes: US large stocks, US small stocks, EAFE Equity, EM Equity, and REITS. The corresponding benchmark weights are: US large stocks: 30% US small stocks: 5% EAFE equity: 35% EM equity: 25% REITS: 5% (Europe, Australasia, and Far East) (Emerging Markets) (Real Estate Investment Trusts) The spreadsheet HW4_Q1 has your estimates for the annual expected return (*not* expected active return) E(r) and volatility o of each asset class, as well the correlation of returns for all pairs of asset classes. To save time, an incomplete covariance matrix V based on such estimates is also provided. a) Find your estimates for the vector of Expected Active Returns E[a] and complete the covariance matrix of returns V. (Hint: Start by finding the benchmark's expected return) b) Find the optimal portfolio for a target Active Risk of 5% per year, assuming that short-positions are allowed. What is the Information Ratio of such portfolio? What is the beta of the optimal portfolio with respect to the benchmark? c) What is the probability that the optimal portfolio you found in b beats (i.e., outperform) the benchmark? d) What is the probability that the optimal portfolio you found in b has negative returns? Note that, contrary to item c, this question is *not* about returns relative to the benchmark. (Hint: The Total Risk or Volatility of a portfolio (different from Active Risk) is wp VWp' ) e) Find the optimal portfolio for a target Active Risk of 5% assuming that short positions are not allowed. What is the Information Ratio of such portfolio? f) Find the optimal portfolio for a target Active Risk of 5% assuming short positions are allowed but constraining the optimal portfolio to have a beta with respect to the benchmark equal to 1? What is the Information Ratio of such portfolio? A 1 Asset Class 2 US Large 3 US Small EAFE Equity 4 5 EM Equity 6 REITS 7 8 9 10 11 12 13 14 15 16 17 18 19 V US Large US Large US Small ?????? EAFE Equity EM Equity REITS B Expected Return (r) Volatility 0.69% -0.15% 4.09% 7.21% 1.27% C 0.0213 ?????? 0.0221 0.0273 0.0233 14.61% 19.46% 17.20% 23.55% 22.14% US Small 0.0379 0.0272 0.0351 0.0330 D Benchmark 0.30 0.05 0.35 0.25 0.05 EAFE Equity 0.0221 0.0272 0.0296 0.0359 0.0262 E Beta wrt benchmark 0.80 1.01 0.97 1.29 0.96 EM Equity 0.0273 0.0351 0.0359 0.0555 0.0326 REITS F 0.0233 0.0330 0.0262 0.0326 0.0490 G Asset Class 1 US Large US Large US Large US Large US Small US Small US Small EAFE Equity EAFE Equity EM Equity H Asset Class 2 US Small EAFE Equity EM Equity REITS EAFE Equity EM Equity REITS EM Equity REITS REITS I Correlation 0.910 0.880 0.795 0.719 0.814 0.766 0.767 0.886 0.688 0.626 J

Step by Step Solution

3.41 Rating (151 Votes )

There are 3 Steps involved in it

Here are the steps to solve this multipart question a Benchmark expected return 30 Er US ... View full answer

Get step-by-step solutions from verified subject matter experts